|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

September 18, 2012 India breaks the FDI shackles: Multi Brand Retail Trading and other sectors liberalized The term TGIF, couldn’t have been given a better description than what the Indian government announced on Friday September 14, 2012. The Cabinet Committee of Economic Affairs (“Cabinet”) approved a series of bold reforms permitting and/or increasing foreign investment in the areas of multi brand retail trading, aviation, broadcasting and power trading exchanges subject to certain conditions. It also pushed forward the disinvestment program. As India navigates through political and economic gridlock these bold set of reforms in the current environment are a step in the right direction. After much debate and deliberation, the Cabinet has approved reforms relating to foreign direct investment (“FDI”) in the certain sectors as follows: 4. FDI limits enhanced in teleports, mobile TV, head end-in-the sky broadcasting service; 5. Foreign investment upto 49 percent permitted in power trading exchanges. Below is a more comprehensive analysis of the reforms. Way forward The country is in need of investment in infrastructure (aviation, power trading exchanges), retail and allied sectors. The Governments’ decision to open up foreign investment in certain sectors will give stimulus to the respective industries. Further, the reforms in the long run will have a mass multiplier effect in improving levels of employment and infrastructure in the country. Having said the above, it is important to note that the above reforms have only been approved by the Cabinet. In order for these to form part of the FDI policy, the same will have to be notified in form of press note/ circulars. Nishith Desai Associates is pleased to present a detailed research paper “Destination India - Welcome Retail” covering in-depth legal, tax and regulatory analysis alongwith industry insight on the Indian retail sector. We will be happy to have your views / comments on our research paper. Please read the disclaimer carefully. Please click here to access the research paper. This document is best viewed in Adobe Acrobat version 7.

- Kartik Maheshwari, Ruchi Biyani, Khushboo Baxi and Vivek Kathpalia You can direct your queries or comments to the authors

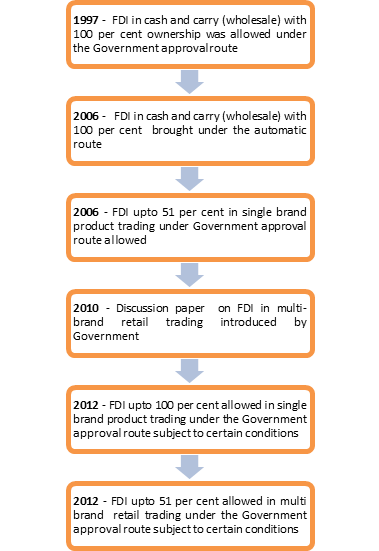

Foreign direct investment in retail trading India entered into the World Trade Organisation’s General Agreement on Trade in Services (“GATS”), in January 1995 pursuant to the Uruguay Round negotiations. One of the commitments to the GATS includes wholesale and retailing services and therefore India was under an obligation to open up the retail trade sector to foreign investment. The retail sector in India is considered to be an economic and politically sensitive sector especially since it impacts a large number of the population comprising farmers, small traders and the economies that surround them. The Government has therefore been liberalizing its FDI policy in retail trading in a phased manner as reflected in the diagram below:

· Multi brand retail trading Till now, FDI in multi-brand retail trading was not allowed. The current policy does not define the term ‘multi brand’. Simply put, multi brand retail trading implies the sale of multiple brands under one roof to retail customers for personal consumption. The Cabinet has now approved FDI in multi brand retail trade up to 51%, with government approval. The proposal to allow FDI in multi brand retail trading dates back to July 2010, when Department of Industrial Policy and Promotion (“DIPP”) first introduced its discussion paper1 on allowing FDI in multi-brand retail. The proposal of allowing FDI in multi brand retail was then approved by the Cabinet in November 2011. However, due to adverse political backlash, the proposal was kept on hold. The press release of the government lists out the following conditions with respect to FDI in this sector: 1. Retail sales outlets may be set up in those States which have agreed or agree in future to allow FDI in multi brand retail trade Under List II of Seventh Schedule of the Constitution of India, trade and commerce within a State is a State subject. A national legislation to govern retail sector, consequently, needs the approval of the States under the Constitution. As of now, only State Governments of Delhi, Assam, Maharashtra, Andhra Pradesh, Rajasthan, Uttarakhand, Haryana, Manipur and the Union Territory of Daman & Diu and Dadra and Nagar Haveli have supported the Cabinet proposal. Accordingly, it would be the prerogative of the State Governments to decide whether and where a multi-brand retailer, with FDI, is permitted to establish its sales outlets within the State. The establishment of the retail sales outlets will have to be in compliance with applicable State laws/ regulations, such as the Shops and Establishments Act etc. Additionally, the companies engaged in multi brand retail trading will also have to comply with local zoning regulations, warehousing requirements, access, traffic, parking and other logistics as prescribed by State Governments from time to time. Implication: With this restriction, each investor will have to comply with policy on FDI at both Centre and State levels. Depending on State policy on multi brand retail trade, the investors may or may not be permitted to invest in those States. Interestingly this seems to be the first time that discretion on whether to permit FDI in a sector or not has been left to the States .It speaks volumes of the growth in power of the States in India. 2. Retail sales locations may be set up only in cities with a population of more than 1 million The reach of retail sales outlets of foreign multi brand retail trader will be limited to only those cities with a population of 1 million (including an area of 10 kilometers around the municipal/urban agglomeration limits of such cities). As per 2011 Census only 53 cities qualify for FDI in multi-brand retail locations. In the current regime, 100% FDI is allowed upto wholesale cash and carry point from which franchise/small retailers are able to source quality products for sale to the public at large. On the other hand, States/ Union Territories, which do not have any city with a population exceeding 10 lakhs, but are desirous of implementing the policy, would have the flexibility to do so of identifying the largest city where FDI could be allowed. Implication: The above restriction of establishment of retail sales outlets in cities with a minimum prescribed population would limit reach of foreign investor. However, the current restriction to Tier 1 and Tier 2 cities seems reasonable given the sensitivity around the sector and prevalent undeveloped / unorganised retail in small towns/ villages which would be unable to compete with large players. 3. Minimum amount to be brought in, as FDI, by the foreign investor, would be US$ 100 million. The foreign investor has to bring in a minimum investment of USD 100 million in an entity engaged in multi brand retail trading. Implication: Retail sector being a capital intensive sector, the requirement for minimum capitalisation appears logical. This will attract serious investors and allow the government to study the benefit such investment will have on the Indian economy. 4. 50% of total FDI brought in to be invested in `backend infrastructure` within three years Considering the need for investment in back end infrastructure in the country, at least 50% of total FDI brought in is required to be invested in 'backend infrastructure' within three years of the induction of FDI. Investment in ‘back-end infrastructure’ will include capital expenditure on all activities such as investment made towards processing, manufacturing, distribution, design improvement, quality control, packaging, logistics, storage, warehouse, agriculture market produce infrastructure etc. Expenditure incurred on front-end units, land cost and rentals will not be reckoned for purposes of backend investment. Implication: The Indian retail sector is fraught with lack of adequate infrastructure and increased cost and wastage due to disrupted supply chains and middlemen. To address this problem, the requirement for investment in back end infrastructure within a three year timeframe has been introduced. 5. 30 percent mandatory local sourcing requirement Similar to the requirement of mandatory local sourcing as applicable in single brand product trading (prior to Cabinet meeting) at least 30% of the procurement of manufactured/ processed products shall be sourced from `small industries`2. Compliance with this condition will have to be self-certified by the company and then cross-checked by statutory auditors. Implication: In case of single brand product trading, this condition was seen as a big hurdle. While the condition has been modified in case of single brand product retail trading, anomalies still remain (see discussion below on amendment to this condition and its implication). The mandatory local sourcing requirement in case of multi brand retail trade is aimed to provide a boost to small industries. It may be easier for Multi Brand product retailers to meet this condition since they have a large spectrum of goods to offer. · Single brand product retail trading FDI upto 100% is permitted in Single-Brand Product Retail Trading under the government route subject to fulfillment of certain riders as introduced in January 2012. For more details please refer to our hotline on “100% Foreign Direct Investment in Single Brand Retail allowed!!! In this regard, we understand that certain foreign investors had raised concerns with respect to compliance with these conditions. After much debate and deliberation, these conditions have now been diluted / modified as follows: 1. Brand ownership by foreign investor either directly or under licensing/ franchise/sub-licence arrangements The condition requiring the foreign investor to be the owner of the brand was introduced under the FDI policy issued by the DIPP on September 30, 2011. Once again this condition was seen to be restrictive as it ignored the IP holding structures prevalent globally. This condition has now been modified pursuant to which only one foreign investor whether owner of the brand directly or under a licensing/ franchise/sub-licence agreement, shall be permitted to invest in single brand product retail trading in the country, for the specific brand for which approval is being sought. The onus for ensuring compliance with this condition shall rest with the Indian entity carrying out single-brand product retail trading in India. The investing entity shall provide evidence to this effect at the time of seeking approval, including a copy of the licensing/ franchise/sub-licence agreement, specifically indicating compliance with the above condition. Implication: The dilution of the above condition is in line with international best practices and IP holding structures. It should provide the right fillip to investment in this sector. 2. Local 30 percent sourcing requirement modified The Press Note 1 of 2012 dated January 10, 2012, permitted FDI, up to 100%, in single brand product retail trading and provided that in respect of proposals involving FDI beyond 51%, mandatory sourcing of at least 30% of the value of products sold would have to be done from Indian 'small industries/ village and cottage industries, artisans and craftsmen'. While the mandatory 30% local sourcing requirement continues, the policy framework now provides that sourcing in India should be preferably made from MSMEs (micro, small and medium enterprises), village and cottage industries, artisans and craftsmen, in all sectors, where it is feasible. This condition will have to be complied by the company incorporated in India carrying out single-brand product retail trading and recipient of FDI. Implication: The fine print of the above modification by way of circular is yet to be notified, therefore, it needs to be seen to what extent the requirement has been technically modified. The press release of the Cabinet meeting acknowledges that the wide range of products that may be made available under single brand (specialized/ niche products to general category). Therefore, to the extent it is feasible in case of a sector, 30% of the value of the goods purchased shall be sourced preferably MSMEs, village and cottage industries, artisans and craftsmen. It is important to note the term MSME has not been defined. Further, the press release also underlines the foreign retail traders finding it difficult to meet local sourcing requirements would have to build production capabilities either in existing or new units so as to cater to their requirements in terms of design, production, quality etc. Foreign direct investment in aviation Given the grim state of affairs of the aviation sector, the Cabinet has allowed foreign airlines to make foreign investment in scheduled and non-scheduled air transport services upto 49 percent (cumulative under both FDI and FII investment route). Until now, foreign airlines were allowed to participate in the equity of companies operating cargo airlines, helicopter and seaplane services, but not in the equity of an air transport undertaking operating scheduled and non-scheduled air transport services. The Cabinet has now permitted foreign airlines to invest, under the approval route, in the capital of Indian companies operating scheduled and non-scheduled air transport services, up to the limit of 49 percent of their paid up capital. In addition to compliance of securities law regulations in case of investment in a listed scheduled operator, such investment would further be subject to the conditions that: - Scheduled Operator’s permit can be granted only to a company: a. That is registered and has its principal place of business within India, b. The Chairman and at least two-thirds of the directors of which are citizens of India, and c. The substantial ownership and effective control of which is vested in Indian nationals. - All foreign nationals likely to be associated with Indian Scheduled and Non-Scheduled air transport services shall be subject to security clearance before deployment; and - All technical equipment that might be imported into India, as a result of such investment, shall require clearance from the relevant authority in the Ministry of Civil Aviation. Implication: The aviation sector is one of the major economic drivers for prosperity, development and employment in a country. However, of late the sector is facing a debt crisis. In order to rejuvenate the sector, the Government recently increased the limit of external commercial borrowing in the aviation sector subject to certain conditions. The liberalization of foreign policy in scheduled and non-scheduled air transport services will further allow the players to rejig their affairs. It is important to note that the current reforms now allow strategic investors to enter Indian aviation sector as opposed to financial investors. Further, the strategic investor will require a 51% Indian partner and will have to be dependent on the same. Foreign direct investment in broadcasting The Cabinet, vide a press release3 issued on September 14, 2012 has approved the long standing demand of the broadcasting industry to raise the limit of foreign investment in companies operating in the broadcasting sector from 49% to 74%. The Cabinet has based its decision on the rationale that enhanced access to foreign investment would enable the expansion of the reach of broadcasting services and to make the foreign investment policy for the broadcasting sector consistent with that of the telecom sector, due to the convergence of technologies involved in these two sectors. The following changes are proposed to be brought into effect: i. Teleports (setting up uplinking HUBs/Teleports): Direct to Home (DTH); Cable Networks (Multi-System-Operators (MSOs) operating at National or State or District level and undertaking upgradation of networks towards digitalization and addressability): Under the extant Foreign Direct Investment (“FDI”) Policy, foreign investment up to 49% is permitted in the aforementioned activities. It has now been decided to increase the foreign investment limit from 49% to 74%. However, this increase in threshold for investment would be permitted up to 49% under the automatic route whereas investments beyond 49% and up to 74% will be permitted under the government approval route (i.e., the approval from the Foreign Investment Promotion Board (“FIPB”) will be required). Importantly, it has been clarified that in respect of Cable Networks i.e., MSOs not undertaking up-gradation of networks towards digitalization and addressability and Local Cable Operators, the existing foreign investment limit of 49% under the automatic route would continue to apply. Implication: As far as the increase in the DTH and MSO segment (provided the MSOs undertake upgradation of networks towards digitalization with addressability) is concerned, it will result in a big boon for these players and seems to be the right way forward in light of the impending deadline for digitization and the need for urgent capacity building at all levels. The press release also states that the MSOs that do not intend to undertake up-gradation of networks towards digitalization and addressability will continue to maintain their foreign investment limits at 49%. It may be noted that digitization is required to be implemented phase-wise in various cities. Therefore, in this case, it could be construed that the MSOs who have not yet undertaken the process of up-gradation of networks will need to be restricted to foreign investment at 49% until the time they begin undertaking such up-gradation towards digitization. It needs to be seen, though, if there is any further clarity being provided in this respect. ii. Mobile TV: The extant FDI Policy does not prescribe any limit for investment connected with mobile television; however it has now been decided to permit foreign investment up to 74%, with the similar rider as is applicable to DTH and Cable Networks, i.e. foreign investment up to 49% would be permitted under the automatic route whereas investments beyond 49% and up to 74% will be permitted under the government approval route. There is no definition of mobile television that has been provided under this press release, however, in 2007, TRAI had issued a consultation paper4 on issues relating to Mobile Television Service, referred to mobile television service as provision of television services to subscribers for viewing on handheld or portable devices via mobile telecommunication networks or by using the broadcasting technologies. It is this mobile television service using the broadcasting technologies that is proposed at a 74% foreign investment limit. Implication: The current FDI policy currently only prescribes limits of 74% foreign investment in telecom networks (for mobile television services). It now appears that the Cabinet believes that mobile television is poised to be a new medium for dissemination of information and has therefore placed a cap of 74% of foreign investment for carriage of mobile television service via broadcasting networks. Therefore, for instance, a telecom service operator who intends to provide mobile television services for carriage via the broadcasting networks can obtain foreign investment up to 74% which is at par with the telecom services related activities being carried out. Though there has been a consultation paper and subsequent recommendation in connection with mobile television service, specific guidelines to this effect yet remain to be implemented. iii. Headend-in-the Sky (“HITS”) Broadcasting Service: The existing limit of 74% foreign investment (whereby up to 49% would be permitted under the automatic route and investments beyond 49% and up to 74% will be permitted under the government approval route) will continue to apply for this service. Foreign investment, in companies engaged in all the aforementioned services, will be subject to sectoral and security conditions and guidelines, as may be specified from time to time, by the concerned Ministries. iv. Uplinking / Downlinking of ‘News & Current Affairs’ TV channels and ‘Non-news & Current Affairs’ TV channels; FM Radio: There has been no change in the foreign investment limits for uplinking / downlinking and for FM Radio. The existing limit of 26% foreign investment, under the government approval route, would continue for uplinking of ‘News & Current Affairs’ TV channels and for FM Radio. For uplinking of ‘Non-News & Current Affairs’ TV Channels / Downlinking of TV Channels, the existing policy of 100% foreign investment, subject to government approval, would also continue. v. Calculation of Foreign Investment Unlike the companies operating in the telecom sector, where the calculation of the direct foreign investment limit includes FDI, investment by Foreign Institutional Investors (“FIIs”), Non Resident Indians (“NRIs”), Foreign Currency Convertible Bonds (“FCCBs”), American Depository Receipts (“ADRs”), Global Depository Receipts (“GDRs”) and convertible preference shares held by foreign entities, there has not been such consistency for companies operating in the broadcasting sector, and for each segment under it the foreign investment limits include different components. Vide this press release, though, it has been decided to rationalise the methodology of calculation of direct investment and to bring about the methodology in the broadcasting sector at par with the telecom sector. Accordingly, it has been decided that the foreign investment limit in companies engaged in various activities of the providing carriage services (except cable services) will include, in addition to FDI, investment by FIIs, NRIs, FCCBs, ADRs, GDRs and convertible preference shares held by foreign entities. Implication: With respect to the new method of calculation of foreign investment, TRAI had, earlier, recommended different foreign investment limits for companies engaged in providing 'carriage' and 'content' services. The services such as teleports, DTH, HITS, Mobile TV, IPTV and Cable TV come under broadcasting carriage services. Television Broadcasting, i.e., Uplinking and Downlinking, and FM Radio come under broadcasting content services. Therefore, the intention, at this point, of the government appears to be in connection with investments in the DTH, HITS Mobile TV and IPTV segments (since Cable services have been carved out as an exception), though, the press release does not provide much clarity on this point. The Telecom Regulatory Authority of India (“TRAI”) had, initially, issued its recommendations on foreign investment limits for the broadcasting sector in April 2008. However, subsequently, as a result of a change in the methodology for assessment of foreign investment in Indian companies, TRAI issued a fresh set of recommendations in June 2010. These recommendations were brought about in light of the increasing convergence of technologies in the telecom and the broadcasting sectors, the need for uniformity amongst both these sectors, and consequently, to enable the provision of broadcasting carriage services, by not only using the broadcasting networks but also the telecom networks. The rationale being that, it is possible for cable TV networks to provide voice telephony and broadband (including Internet). Similarly, the modern telecommunications networks are also capable of triple play, i.e. offering voice, video and data services and the terms and conditions of Unified Access Service License (UASL) and Cellular Mobile Telephone Service (CMTS) license agreements already permit the same. The increased FDI caps in the broadcasting sector as per the Cabinet’s approval appear to be in line with the TRAI recommendations of June 2010. In view of the changes to the foreign investment limits, the Indian companies engaged in the above-mentioned activities (and where the 74% increase in foreign investment has been brought about) that currently have investments up to 49% and who now intend to bring in additional investments up to 74% will now require approaching the FIPB for prior approval. Such entities will, perhaps, also need to obtain approvals from the MIB (under the respective applicable regulations) as a change in the shareholding will have occurred. Foreign direct investment in power trading exchanges The Cabinet has permitted foreign investment upto 49 percent (FDI limit of 26 per cent and FII limit of 23 per cent of the paid-up capital], in power trading exchanges, in compliance with SEBI Regulations; Central Electricity Regulatory Commission (Power Market) Regulations, 2010; and other applicable laws/ regulations; security and other conditionalities. FII investments would be permitted under the automatic route and FDI would be permitted under the government approval route. This is subject to the conditions that FII purchases shall be restricted to secondary market only, and no non-resident investor/ entity, including persons acting in concert, holding more than 5 percent of the equity in these companies.

___________________ 1 Discussion Paper on FDI in Multi Brand Retail Trading, http://dipp.nic.in/DiscussionPapers/DP_FDI_Multi-BrandRetailTrading_06July2010.pdf 2 Small industries mean industries which have a total investment in plant & machinery not exceeding USD 1 million. This valuation here refers to the value at the time of installation, without providing for depreciation. Further, if at any point in time, this valuation is exceeded, the industry shall not qualify as a `small industry` for this purpose. 3 http://pib.nic.in/newsite/erelease.aspx?relid=87787 4 Available at http://trai.gov.in/WriteReaddata/ConsultationPaper/Document/cpaper18sep07.pdf. Recommendations were, subsequently received from MIB and again, from TRAI (to MIB’s recommendations) in 2008 and 2010 respectively.

****************

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||