Deal Talk

January 23, 2025

“Driving” Into the Future Together: Unpacking Indian Law Considerations for The Proposed Honda-Nissan Partnership

Introduction

On December 23, 2024, Japan’s second and

third largest carmakers respectively, Honda Motor

Co., Ltd (“Honda”)

and Nissan Motor Co., Ltd (“Nissan”)

sent shockwaves through the automotive industry

when they announced the signing of a memorandum

of understanding (“MOU”)

to consider business integration, through the establishment

of a joint holding company, for “deepening

the framework of” their existing strategic

partnership.1 This follows another MOU

that was previously executed by the parties on August

1, 2024 for achieving carbon-neutrality and zero-traffic-fatality

in the automotive industry.

While strategic alliances in the automative industry

are common, this mega-alliance is poised to alter

the dynamics of the global automotive industry by

creating the third largest automaker in the world.2

Additionally, Nissan and Honda have chosen a non-conventional

model for a partnership in the automotive industry

(as compared to the more conventional models such

as acquisitions, mergers, platform sharing or technology

sharing). This commitment from Honda and Nissan

also comes in the backdrop of increasing competition

from Chinese counterparts, with Honda’s chief

executives indicating that this partnership is part

of a plan to stabilise operations by 2030.3

Interestingly, there are public announcements that

subject to discussions between parties, the merger

may potentially include Mitsubishi Motors Corp.

(of which Nissan is a major shareholder).

In our inaugural Deal Talk for 2025, we break

down all the implications under Indian law for a

deal similar to the Honda-Nissan deal structure,

highlighting critical considerations to be borne

in mind by two industry conglomerates when coming

together overseas whilst having substantial presence

in India.

Proposed Transaction

Honda and Nissan are Japanese listed companies

that have signed the MOU to create a joint holding

company incorporated in Japan, which shall operate

as the parent company of both the companies and

be listed (by way of a “technical listing”)

on the Prime Market of the Tokyo Stock Exchange

(“TSE”) (such company,

the “Joint Holding Company”).

A “technical listing” is governed by

Rule 208 of the Securities Listing Regulations of

the TSE, which provides companies with the flexibility

to list existing shares on public markets instead

of issuing new shares to the public under the traditional

initial public offering route. The ability to undertake

a “technical listing” is available only

when a company meets the criteria set out in Rule

209, which broadly assesses the market capitalisation,

number of shareholders, and overall financial performance

of the listed company. An interesting point to note

is that Indian securities market does not have an

institutionalized concept of a “technical

listing”.

Post incorporation, the Joint Holding Company

shall hold the entire shareholding of Nissan and

Honda which would therefore become wholly owned

subsidiaries of the Joint Holding Company. To this

extent, both Nissan and Honda will respectively

delist from TSE as a part of this process. While

the date of listing of the Joint Holding Company

and delisting of Honda and Nissan will be determined

according to the applicable law, at the time when

the Joint Holding Company acquires the shares of

Nissan and Honda, existing public shareholders of

Nissan and Honda would have the ability to swap

their shares in Nissan and Honda with the shares

of the Joint Holding Company.

However, the share transfer ratio has not been

finalised and is slated to be determined subject

to due diligence and third-party valuations referring

to average closing prices of Honda and Nissan prior

to the public announcement of the MOU.

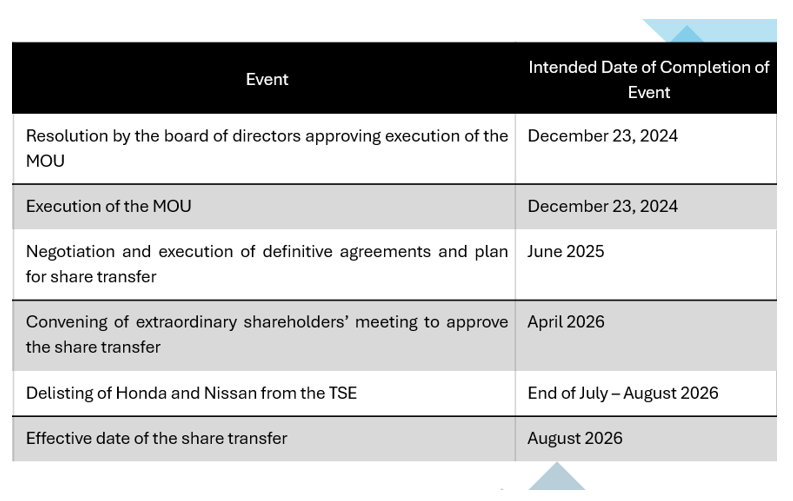

The broad timelines and step plan for this deal

are as follows –

(the “Proposed Transaction”).

Once the Proposed Transaction is consummated,

on the effective date of the share swap, Honda will

nominate a majority of the internal and external

directors of the Joint Holding Company. Further,

it is envisaged that the president and representative

director or president and representative executive

officer of the Joint Holding Company will be selected

from amongst Honda’s nominated directors.

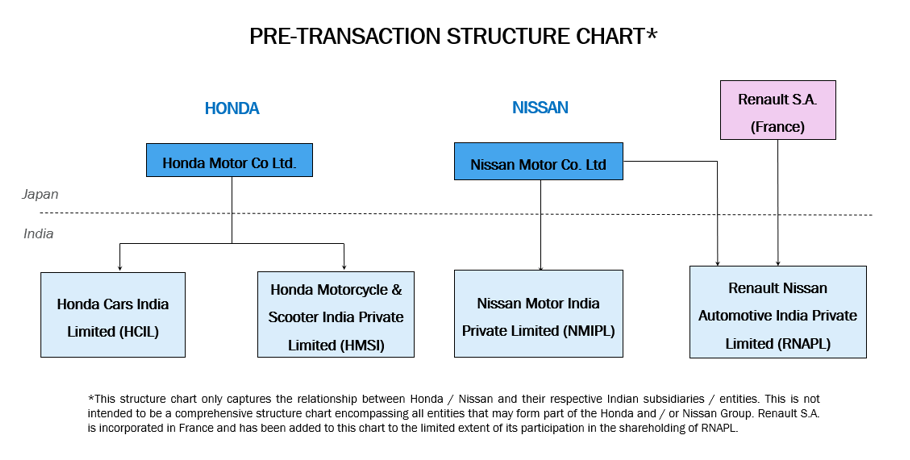

A diagrammatic representation of the current

group structures of Honda and Nissan, and the structure

pursuant to the Proposed Transaction is as follows –

India-centric deal considerations

for the parties

Presence of Honda and Nissan in India’s

automotive sector

(i)

Honda

As per public sources, Honda majorly operates

through two companies in the Indian automotive market:

(a) Honda Cars India Limited (“HCIL”),

a public limited company operating as a wholly owned

subsidiary of Honda,4 and (b) Honda Motorcycle &

Scooter India Pvt. Ltd. (“HMSI”),

a private limited company also operating as a wholly

owned subsidiary of Honda.5

(ii)

Nissan

Public sources indicate that in a structure similar

to that of Honda, Nissan’s Indian presence

in the automobile industry is majorly through Nissan

Motor India Pvt Ltd (“NMIPL”),

which is a wholly owned subsidiary of Nissan.6

Further, Nissan has an alliance with French carmaker

Renault in India. Renault Nissan Automotive India

Private Limited (“RNAPL”)

is a joint venture between Renault and Nissan which

undertakes manufacturing of import and export vehicles

for each of them.

Considerations from an Indian legal perspective

While we wait for finalisation of the deal structure

and a copy of the MOU to be disclosed in the public

domain, from an Indian law perspective, the Proposed

Transaction will likely involve an indirect transfer

of the entire shareholding of HCIL, HMSI and NMIPL

from Honda and Nissan to the Joint Holding Company.

However, based on the structure available as of

now, below are some of the critical Indian law considerations

that the parties may need to bear in mind7

while undertaking a structure similar to the Proposed

Transaction –

Potential

approval of the Competition Commission of India

(“CCI”) under the

Competition Act, 2002 (“Act”)

As per recent amendments to the Act effective

since September 10, 2024, any transaction meeting

the following criteria will be subject to the prior

approval of the CCI before consummation: (i) the

value of the transaction is INR 2,000 crores (i.e.

approximately USD 231 million) or more (“Value

Test”); and (ii) the target has “substantial

business operations” in India, (“Business

Test”) each as per the manner set

out in the Competition Commission of India (Combinations)

Regulations, 2024 (collectively, the “Deal

Value Threshold”). The Deal

Value Threshold is applicable even if the target

otherwise meets the de minimis target exemptions

under the Act, which exempts notifiability of transactions

where the target’s assets or turnover are

below specified limits.8 Exemption can

be sought from notification arising on account of

the Deal Value Threshold only if an exemption is

available under the Competition (Criteria for Exemption

of Combinations) Rules, 2024.

While the deal value for the Proposed Transaction

is not available in the public domain, the parties

believe that this integration will lead to sales

revenue exceeding 30 trillion yen (approximately

USD 191.4 billion) and operating profit of more

than 3 trillion yen.9

In light of the above, in the event the Proposed

Transaction passes both the Value Test and the Business

Test, it would be required to be notified to the

CCI.

If prior approval of the CCI is to be sought

owing to the Deal Value Threshold, the Joint Holding

Company (being the acquirer in the Proposed Transaction)

will have to file an application with the CCI upon

execution of transaction documentation (and prior

to the consummation of the Proposed Transaction)

seeking its approval. Depending on the extent of

overlaps in the Indian market between the parties

to the Proposed Transaction, the process of receiving

approval from the CCI could either be through the

green channel route or may take 30-40 days.

While scrutinising the application, the CCI may

potentially also examine the following indicative

factors to assess whether the Proposed Transaction

leads to an “appreciable adverse effect

on competition” in the Indian markets:

Potential market concentration

of Honda and Nissan in India pursuant to the

Proposed Transaction and their joint market

power, in all relevant product markets such

as non-electric automobiles, electric automobiles,

four-wheelers and two-wheelers markets, to assess

dominance; Possibility of vertical

and horizontal integration with dealers, suppliers

and servicing agencies involved in the automotive

sectors; Benefits to end-customers

through this deal.

However, given that the Indian automobile market

is saturated with multiple players, the potential

of the Proposed Transaction causing an “appreciable

adverse effect on competition” would

be relatively lower.

Possibility

of incurring indirect transfer tax under the

Income Tax Act, 1961 (“IT Act”)

An indirect transfer occurs when the effective

control of securities held in a specific jurisdiction

occurs indirectly as a result of a transfer

of ownership / interest of its holding entity (and

not directly as a result

of an actual transfer of securities in that specified

jurisdiction).

Under the IT Act, any income arising from an

indirect transfer of shares is taxable as capital

gains if the foreign entity derives its value “substantially”

from the assets situated in India.10

Value is said to have been derived “substantially”

from Indian assets if the value of such assets:

(i) exceeds INR 10 crores (approx. USD 1.15 million)

(“Limb 1”);

and

(ii) represents at least 50% of the value of all

assets owned by the company or entity (“Limb

2”). It is important to note that

both Limb 1 and Limb 2 will have to be met for indirect

transfer tax to be levied on a transaction.

Therefore, in the event the asset value of HCIL

and HMSI (for Honda) and NMIPL (for Nissan) is above

INR 10 Crores (approx. USD 1.15 million) each and

respectively for Honda and Nissan, they represent

more than 50% of their global value of assets, then

the transfer of shares of Honda and Nissan from

the current shareholders to the Joint Holding Company

could trigger indirect transfer tax in India.

The methodology for calculation of the asset

value of the entity in India has been prescribed

in Rule 11UB of the Income Tax Rules, 1962. Limb

1 will involve calculation of the current fair market

value of the shares held by Nissan and Honda in

HCIL, HMSI and NMIPL respectively through the prescribed

valuation methodology to check if its value exceeds

INR 10 crores. On the other hand, assessment of

Limb 2 will involve: (i) identification of the fair

market value of each of Nissan and Honda as per

the prescribed methodology; (ii) identification

of the fair market value of HCIL, HMSI and NMIPL

as per the prescribed methodology; and (iii) subsequent

comparison whether the 50% threshold is met based

on the fair market values calculated in (i) and

(ii).

It is important to note that the instance of

the indirect transfer tax under the IT Act would

be on the hands of the ‘sellers’ of

shares of Honda and Nissan (i.e. the existing shareholders).

However, an important point to note here is that

the Income Tax Rules, 1962 also provides for a ‘Small

Shareholder Exemption’ from indirect transfer

tax which provides that indirect transfer tax shall

not apply if the non-resident, directly or indirectly,

does not

hold (i) the right of management or control (including

a right which would entitle the person to the right

of management or control) or (ii) voting power,

share capital or interest exceeding 5% of the total

voting power, share capital or interest (as the

case may be) of the company or entity which directly

owns the assets situated in India.

Therefore, for any transaction which follows

a similar structure to the Proposed Transaction

shall also undertake the analysis for indirect transfer

tax in India.

Press

Note No. 3 of 2020 (“PN3”)

considerations

Since (i) the ultimate holding company of HCIL

and HMSI will change from Honda to the Joint Holding

Company; and (ii) the ultimate holding company of

NMIPL will change from Nissan to the Joint Holding

Company, it will amount to an indirect investment

of the Joint Holding Company into the existing Indian

entities of Honda and Nissan. As an effect of this

indirect investment, the beneficial owner

of the shares of the Indian companies will change

to the Joint Holding Company.

PN3 bars investments into India from entities

that share land borders with India, or where the

beneficial owner of an investment into India is

situated in or is a citizen of any such country

sharing land borders with India. These countries

include China (along with Hong Kong), Bangladesh,

Afghanistan, Nepal, etc.

Accordingly, as a result of the Proposed Transaction,

the parties will have to ensure that the beneficial

owner of the Joint Holding Company is not situated

in / a citizen of a land bordering country. Since

the Joint Holding Company shall be a listed company,

it may also be important to undertake this assessment

with respect to the existing shareholders of Honda

and Nissan that would have been a shareholder of

Honda or Nissan prior to the PN3 coming into force

(that shall become shareholders of Joint Holding

Company as a result of the Proposed Transaction).

The ‘significance’

of the Significant Beneficial Owner (“SBO”)

under the Companies Act, 2013 and allied rules

(“CA 2013”)

Under the CA 2013, it is mandatory for every

legal holder of shares to declare the holder of

beneficial interest (i.e. SBO) in such shares to

the Indian company, if such beneficial interest

is not held by them.11 Further, Indian

companies are required to subsequently disclose

these beneficial owners to the Registrar of Companies

(“ROC”).12

Considering that HCIL, HMSI and NMIPL are wholly

owned subsidiaries, the currently reported SBOs

for each of these entities are likely to be the

controlling shareholders of Honda and Nissan respectively.

This analysis would be required to be undertaken

again to assess if there has been any change in

the SBO by virtue of the Proposed Transaction. In

case of a change, HCIL, HMSI and NMIPL may have

to file an updated Form BEN-2 (based on the declaration

provided to it by the Joint Holding Company in Form

BEN-1) with the ROC to reflect the new SBO.

Recent orders from the ROC in the LinkedIn and

Samsung cases suggest that foreign managing officials

of the ultimate foreign holding company could be

considered “significant beneficial owners”

of Indian subsidiary companies (regardless of whether

they directly or indirectly, through the entity,

control the affairs and management of the Indian

company), and be penalised for non-declaration.13

Therefore, in light of these developments, the assessment

and resultant categorisation of the SBO must be

conducted with due consideration to the resultant

group structure dynamics.

Overseas

investment considerations applicable to resident

Indians holding securities of Nissan or Honda

(on the Japanese stock exchange)

Another key consideration for the Proposed Transaction

is the potential impact of Indian overseas investment

laws on the Indian resident shareholders of the

foreign parent companies (being the listed Nissan

and Honda entities in Japan). This may also be relevant

for Indian employees of Nissan and Honda, who may

have acquired shares in the Japanese listed entities

through employee stock ownership plans / employee

benefit plans.

The Foreign Exchange Management (Overseas Investment)

Rules, 2022 (“OI Rules”)

govern investments by Indian residents into overseas

entities. Under Schedule III read with Rule 13 of

the OI Rules, a resident individual may make or

hold overseas investments via a “swap

of securities”

only

in cases of a merger, demerger, amalgamation, or

liquidation. Thus, the OI Rules do not permit Indian

residents to acquire shares of an overseas entity

through a share swap, unless the swap arises from

one of these specific transactions.

Therefore, the parties must evaluate whether

there are any Indian resident shareholders of Honda

and Nissan as on date and implement suitable tax

and legal structuring to ensure that the Proposed

Transaction complies with Indian laws while providing

the same commercial benefits to such shareholders.

Contractual

obligations with respect to “change in

control” triggers under contracts executed

by HCIL, HMSI, and NMIPL

A critical consideration in the Nissan-Honda

deal is the assessment of whether a “change

in control” obligation will be triggered

under contracts executed by each of HCIL, HMSI and

NMIPL (including but not limited to with lenders,

vendors, customers and suppliers).

Since the Proposed Transaction could result in

an ultimate change in control for the Indian subsidiaries

of both Nissan and Honda, the parties may have to

conduct a thorough analysis to determine whether

an indirect “change in

control” is occurring under these agreements,

in order to ensure that HCIL, HMSI and NMIPL discharge

any follow-on obligations arising from this trigger.

These obligations typically include prior notification

to the counterparty and / or obtaining their prior

consent and / or providing post-transaction intimation.

Change in control clauses are particularly prevalent

in lending arrangements entered into by Indian entities,

as they are designed to safeguard the interests

of the creditors.

As mentioned above, beyond financing agreements,

such requirements may also be embedded in vendor,

supplier, or other operational contracts, reflecting

a broad spectrum of potential implications. Addressing

these contractual provisions will be essential to

ensure compliance, avoid disputes, and facilitate

a smooth transition post-deal. Consequently, the

parties may be required to negotiate proactively

with counterparties, negotiate necessary waivers

or approvals, and implement appropriate measures

to satisfy these obligations as per the process

and timelines set out in the underlying agreements.

Conclusion

When structuring a consolidation between foreign

parent companies with Indian wholly owned subsidiaries,

deal teams must go beyond the primary jurisdiction

of the partnership to conduct a detailed analysis

of the Indian regulatory landscape. Ignoring this

critical dimension may result in regulatory hurdles

or missed opportunities for optimizing the structure

of Indian operations.

In light of the ongoing discussions around the

Nissan and Honda partnership in Japan, it is evident

that such collaborations can have significant implications

for Indian subsidiaries. Deal teams should proactively

evaluate Indian laws, including those related to

corporate governance, taxation, foreign exchange

management, and competition, to craft an arrangement

that aligns with both global and local requirements.

A comprehensive approach that balances the strategic

objectives of the parent companies with the regulatory

and operational considerations of their Indian entities

is essential to ensure the consolidation delivers

its intended value seamlessly across all jurisdictions

involved.

Authors

-

Anurag Shah,

Parina Muchhala and

Nishchal Joshipura

You can direct your queries or comments to the relevant member.

1https://global.honda/en/newsroom/news/2024/c241223beng.html.

2https://www.reuters.com/markets/deals/honda-nissan-set-announce-launch-integration-talks-media-reports-say-2024-12-22/.

3https://www.bbc.com/news/articles/cwy3ljvv93lo.

4https://www.aryahonda.com/.

5https://www.honda2wheelersindia.com/about-us/factory.

6https://india.nissanmotornews.com/en-IN/aboutnissanmotorindia.

7Considering that Mitsubishi and Renault’s

involvement in the transaction structure has not

yet been confirmed, we have not added any references

to their Indian presence and impact of the Proposed

Transaction on such entities held by either of them

in India, if any (either standalone or by way of

an alliance).

8The target asset and turnover thresholds

have been analysed in our article here:

https://www.nishithdesai.com/NewsDetails/14949.

9https://global.honda/en/newsroom/news/2024/c241223beng.html.

10Section 9, Income Tax Act 1961.

11Section 89, CA 2013.

12Section 90, CA 2013.

13Please refer to our detailed analysis

of the LinkedIn and Samsung orders at:

https://www.nishithdesai.com/fileadmin/user_upload/Html/Hotline/Yes_Governance_Matters_June1224-M.html.

Disclaimer

The contents of this hotline should

not be construed as legal opinion. View detailed disclaimer.

This hotline does not constitute a

legal opinion and may contain information generated

using various artificial intelligence (AI) tools or

assistants, including but not limited to our in-house

tool,

NaiDA. We strive to ensure the highest quality and

accuracy of our content and services. Nishith Desai

Associates is committed to the responsible use of AI

tools, maintaining client confidentiality, and adhering

to strict data protection policies to safeguard your

information.

This hotline provides general information

existing at the time of preparation. The Hotline is

intended as a news update and Nishith Desai Associates

neither assumes nor accepts any responsibility for any

loss arising to any person acting or refraining from

acting as a result of any material contained in this

Hotline. It is recommended that professional advice

be taken based on the specific facts and circumstances.

This hotline does not substitute the need to refer to

the original pronouncements.

This is not a spam email. You have

received this email because you have either requested

for it or someone must have suggested your name. Since

India has no anti-spamming law, we refer to the US directive,

which states that a email cannot be considered spam

if it contains the sender's contact information, which

this email does. In case this email doesn't concern

you, please

unsubscribe from mailing list.

|

|

We aspire

to build the next generation

of socially-conscious lawyers

who strive to make the world

a better place.

At NDA, there

is always room for the right

people! A platform for self-driven

intrapreneurs solving complex

problems through research, academics,

thought leadership and innovation,

we are a community of non-hierarchical,

non-siloed professionals doing

extraordinary work for the world’s

best clients.

We welcome

the industry’s best talent -

inspired, competent, proactive

and research minded- with credentials

in Corporate Law (in particular

M&A/PE Fund Formation),

International Tax , TMT and

cross-border dispute resolution.

Write to

happiness@nishithdesai.com

To learn more

about us

Click here.

|

|

Chambers

and Partners Asia

Pacific 2024:

Top Tier for Tax,

TMT, Employment,

Life Sciences, Dispute

Resolution, FinTech

Legal

Legal 500

Asia Pacific 2024:

Top Tier for Tax,

TMT, Labour &

Employment, Life

Sciences & Healthcare,

Dispute Resolution

Benchmark

Litigation Asia

Pacific 2024:

Top Tier for Tax,

Labour & Employment,

International Arbitration

AsiaLaw

Asia-Pacific 2024:

Top Tier for Tax,

TMT, Investment

Funds, Private Equity,

Labour and Employment,

Dispute Resolution,

Regulatory, Pharma

IFLR1000

2024: Top

Tier for M&A

and Private Equity

FT Innovative

Lawyers Asia Pacific

2019 Awards:

NDA ranked 2nd in

the Most Innovative

Law Firm category

(Asia-Pacific Headquartered)

RSG-Financial

Times:

India’s Most

Innovative Law Firm

2019, 2017, 2016,

2015, 2014

|

|

|

|