Deal Talk

August 26, 2024

Legacy Reimagined: Godrej Family Restructuring

Introduction

Godrej, a pioneering conglomerate which came

into existence during the Swadeshi Movement in 1897,

is a household name in India, well known across

industries ranging from real estate to consumer

goods. The Godrej group has businesses ranging from

real estate to consumer goods, each of which are

run through multiple group companies.

However, after a 127 year long run, the Godrej

family mutually decided for it to enter into a new

era of operations that are divided amongst the Godrej

families, in a manner which allows the newer generations

to unlock more value from the conglomerate whilst

preserving the goodwill and credibility of the brand.

This arrangement allows the families to independently

run the management and operations of the allocated

entities.

The new era has been innovatively structured

to ensure a smooth division of the entities / existing

businesses in the conglomerate between the existing

patriarch Adi Godrej and his cousin Jamshyd Godrej.

Reorganization

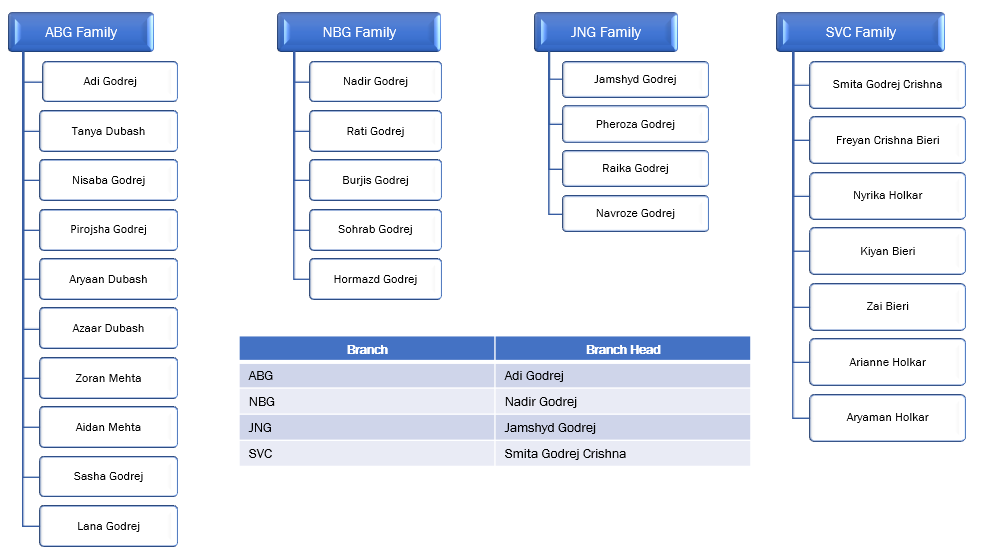

For the purposes of the reorganization, four

family branches were created, with each branch having

a branch head (as set out below). Each member of

the four family branches entered into a Family Settlement

Agreement (‘FSA’) dated

April 30, 2024, to record the restructuring of the

Godrej group companies. Additionally, each member

of the four family branches (other than Pheroza

Godrej and Rati Godrej) also entered into a Brand

and Non-Compete Agreement (‘BNC’)

dated April 30, 2024 to set out terms governing

the adoption, use, ownership and registration of

the ‘Godrej’ brand. None of the Godrej

group companies were party to these agreements.

The family branches and branch heads that have

been created for the reorganization are as follows:

For the purposes of the rearrangement as per

the FSA, the four family branches have been divided

into two groups – (i) ABG – NBG families

have been clubbed together (‘Adi Group’);

and (ii) JNG – SVC families have been clubbed

together (‘Jamshyd Group’).

A brief profile of the companies in the Godrej

group that were divided between Adi Group and Jamshyd

Group are as below:

|

S. No.

|

Name of the Company

|

Listed / Unlisted

|

Key Operation

|

|

1

|

Godrej Industries Limited (‘GIL’)

|

Listed

|

Through its downstream affiliates (GCPL,

GPL, GAVL, GSGL, IMPL, Astec and Anamudi),

GIL’s operations range from fast-moving

consumer goods, real estate, agri-business,

chemicals and financial services.

|

|

2 |

Godrej Consumer Products Limited (‘GCPL’)

|

Listed

|

Affiliate of GIL engaged in the production

and sale of fast-moving consumer goods.

|

|

3 |

Godrej Properties Limited (‘GPL’)

|

Listed

|

Subsidiary of GIL and a real-estate company

developing residential, commercial and township

projects in India.

|

|

4 |

Godrej Agrovet Limited (‘GAVL’)

|

Listed

|

Subsidiary of GIL, which, along with

its subsidiaries, is engaged in agri-businesses.

|

|

5 |

Godrej Seeds and Genetics Limited (‘GSGL’)

|

Unlisted

|

Trading of agricultural products.

|

|

6 |

Astec Lifesciences Limited (‘Astec’)

|

Listed

|

Subsidiary of GAVL engaged in sale of

fungicides, insecticides, herbicides and

intermediates.

|

|

7 |

Innovia Multiventures Private Limited

(‘Innovia’)

|

Unlisted

|

Innovia holds 2.68% shareholding in GPL

and has no other business operations.

|

|

8 |

Anamudi Real Estates LLP (‘Anamudi’)

|

Unlisted

|

Leasing real estates. Further, Anamudi

holds certain investments.

|

|

9 |

RKNE Enterprises

|

Unlisted

|

Management, development, acquisition,

leasing and investment in immovable properties.

Further, it also invests funds of partners

in shares / other forms of investment.

|

|

10 |

Godrej & Boyce Manufacturing Company

Limited (‘G&BMC’)

|

Unlisted

|

Presence across 15 industries through

business units involved in the aerospace,

construction, electricals and electronics,

tooling, storage solutions sectors, etc.

|

|

11 |

Godrej Holdings Private Limited (‘GHPL’)

|

Unlisted

|

Management of investment portfolios of

other companies.

|

|

12 |

Godrej Infotech Limited (‘Infotech’)

|

Unlisted

|

Subsidiary of G&BMC. IT service provider

providing business process consulting, infrastructure

management, implementation, application

support, etc.

|

Division

of group companies between Adi Group and Jamshyd

Group (as per the FSA):

The FSA bifurcates the above-mentioned entities

between the Adi Group and Jamshyd Group, in such

a manner that either family groups are not directly

or indirectly involved in the management or control

of the operations of entities that have been designated

to the other family group.

As per the FSA, Adi Group Entities will, going

forward, be referred to as the ‘Godrej Industries

Group’ and the Jamshyd Group Entities will

be referred to as the ‘Godrej Enterprises

Group’.

Public M&A Considerations

To implement the reorganization

as per the FSA, both the Adi Group and Jamshyd

Group would be required to transfer their shareholding

in the respective entities to the other group. All the listed Godrej

entities fall within the Adi Group Entities

(GIL, GCPL, GPL, GAVL and Astec) and the members

of the Jamshyd Group were required to transfer

shares held by them in the listed Adi Group

Entities to Adi Group members. However, the SEBI (Substantial

Acquisition of Shares and Takeover) Regulations,

2011 (‘Takeover Code’)

requires any acquirer to make an open offer

to the public shareholders if an acquisition

leads to such an acquirer (i) having 25% or

more shareholding or voting rights in a listed

entity or (ii) acquiring control over the listed

entity. In the current case,

the transfer of shares of the listed Adi Group

Entities from Jamshyd Group members to the Adi

Group members would result in triggering the

open offer obligation for Adi Group with respect

to each of the listed Adi Group Entities. However, Regulation

10 of the Takeover Code provides for some general

exemptions to the obligations of an open offer

when the acquirer triggers an open offer. As

per Regulation 10(1)(a)(ii), any acquisition

will be exempted from the obligation of open

offer if such acquisition is pursuant to an

inter-se transfer of shares amongst persons

named as promoters in the shareholding pattern

filed by the target company (as per listing

regulations or the Takeover Code) for not less

than

three

years prior to the proposed acquisition (‘Inter-se

Promoter Exemption’). Both the Adi Group

members and the Jamshyd Group members were disclosed

as promoters in the shareholding pattern of

GIL, GCPL, GPL and GAVL in the previous three

years and therefore, the acquisition by Adi

Group members would fall within the exemption

under the Takeover Code. However, the same was

not true for Astec (an indirect subsidiary of

GIL) as GAVL (which is the parent entity of

Astec) was disclosed as a promoter and neither

the Adi Group members nor the Jamshyd Group

members were disclosed explicitly as the promoters

of Astec over the last three years. Therefore,

this exemption was not available for the acquisition

of indirect control over Astec. This is why on May

2nd,

2024, the Adi Group Members (as acquirers and

persons acting in concert) made an open offer

to acquire 26% shares from the public shareholders

in Astec as per the Takeover Code. Additionally, upon

transfer of the shareholdings held by Jamshyd

Group members to Adi Group members in the listed

Adi Group Entities, the Jamshyd Group members

(along with their Affiliates), currently classified

as promoters of GIL, GCPL, GPL and GAVL, are

required to reclassify themselves as public

shareholders. The process for reclassification

of promoter/promoter group members into public

shareholders is set out in Regulation 31A of

SEBI (Listing Obligations and Disclosure Requirements)

Regulation, 2015. Reclassification is a stock

exchange driven process which includes a board

approval and shareholders’ resolution,

followed by an application to the stock exchange.

Antitrust Considerations

As per Section 6 of

the Competition Act, 2002, any person or enterprise

which proposed to enter into a or proposes to

enter into a combination (where such combination

breaches the thresholds as provided in Section

5 of the Competition Act, 2002) shall give a

notice to the Competition Commission of India

(‘CCI’) upon the

execution of any agreement or other document

for such acquisition. Given that the reorganization

would breach the notifiability thresholds as

per the Competition Act, 2002, both the Adi

Group members and Jamshyd Group members (as

acquirers for their respective entities) notified

the CCI on May 15, 2024. The CCI in its order

dated June 18, 2024, stated that the combinations

notified by the Adi Group and Jamshyd Group

were in the nature of an ‘internal reorganization’

and were not likely to change the market dynamics

in a significant manner. However, the CCI still

undertook an analysis with respect to the linkages

that the other investments (outside the Godrej

group) made by Adi Group and Jamshyd Group would

have with the activities of the Adi Group Entities

and the Jamshyd Group Entities. The CCI was of the

view that the investments of Adi Group within

and outside of the Godrej group had: (a) horizontal

overlaps with Adi Group Entities in the areas

of real estate and development, and (b) vertical

linkages considering the upstream activity of

home automation items and downstream activity

of development and sale of real estate properties. Additionally, the investments

of Jamshyd Group within and outside of the Godrej

group had: (a) horizontal overlaps in real estate,

development and school education services, and

(b) vertical linkages considering the upstream

activity of manufacture and sale of each of:

(i) ready-mix concrete & (ii) wall forming

building materials, and the downstream activity

of real estate and development. However, CCI was of

the view that such overlaps and linkages did

not cause any appreciable adverse effect on

competition given that these overlaps and linkages

could not significantly change the market dynamics

in any plausible market that could be delineated.

Tax Considerations

There have been judicial

precedents to state that divestment of property

(movable or immovable), by individual members/parties

of a family arrangement/settlement to other

members of the family who are party to such

arrangement or settlement, shall not be considered

as ‘transfer’ under Section 2(47)

of the Income Tax Act, 1961, subject to fulfilling

certain conditions as laid down in these precedents

(For ref: Kale V. Deputy Director of Consolidation). It is very important

to note that ‘family arrangements’

not constituting ‘transfer’ under

the Income Tax Act, 1961 is only available as

long as the divestment is by one family member

to another and does not extend to any corporate

entities. Therefore, given that

a ‘family arrangement/settlement’

should not be considered as ‘transfer’

under the Income Tax Act, 1961, it is possible

to take a view that no capital gains should

be applicable on such family arrangement/settlement.

Key Terms of the BNC

In addition to the FSA which provides for the

mechanics of the arrangement mentioned above, the

Adi Group and Jamshyd Group also entered into a

BNC which lays down the roadmap and arrangement

with respect to the brand ‘Godrej’ in

the coming decade (in order to preserve the brand

and prevent confusion amongst consumers), the terms

of which are as below –

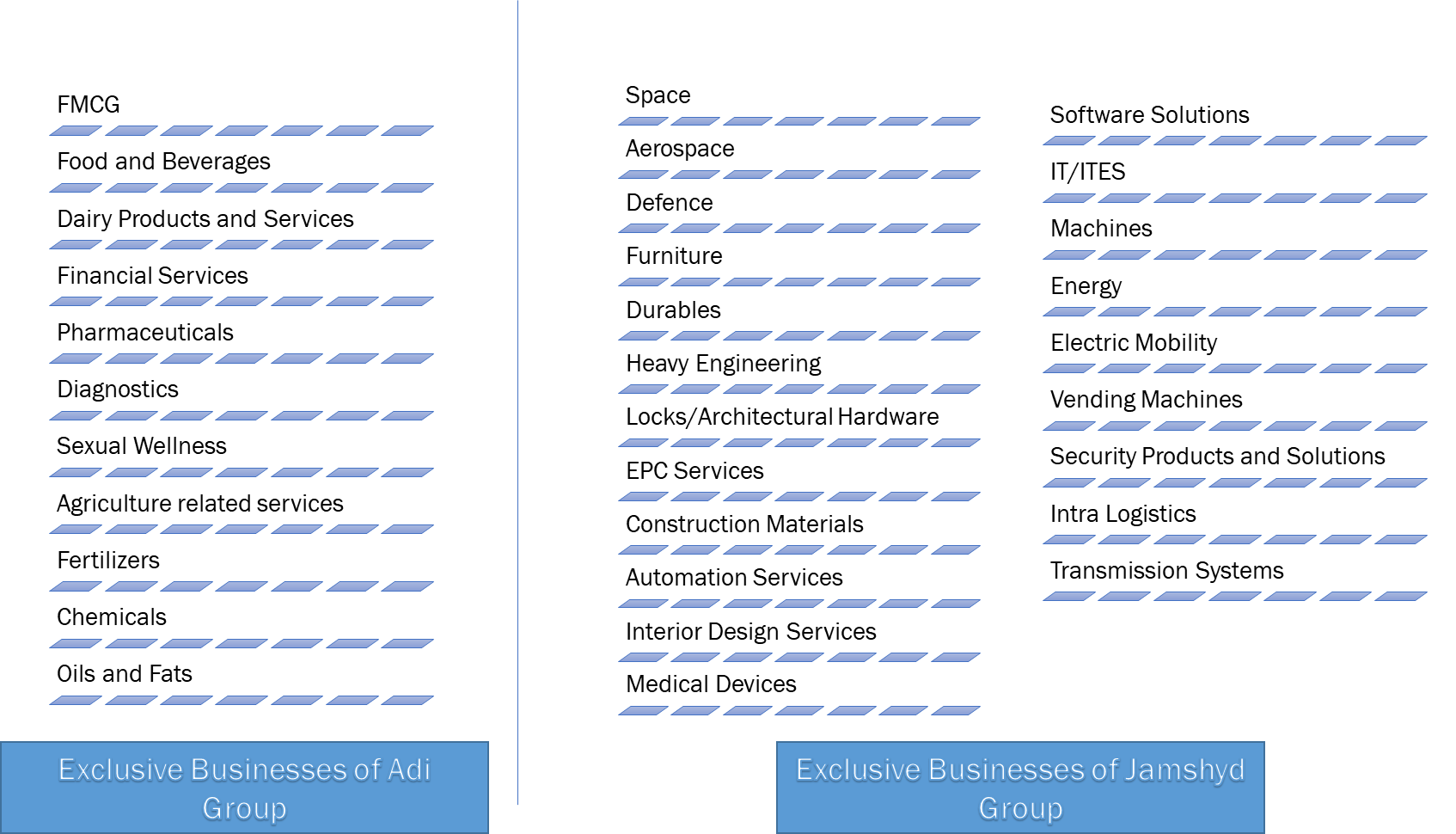

The division under

the BNC can be divided into three segments:

Existing Businesses –

The businesses being undertaken by each

Adi Group and Jamshyd Group as on January

01, 2024

Exclusive Businesses –

Certain businesses of strategic importance

to each Adi Group and Jamshyd Group entity

and the Existing Businesses of such entities.

Shared Businesses –

A list of businesses provided in the BNC

which will be shared by both the family

groups. Also includes any businesses not

falling under Existing or Exclusive Businesses.

The indicative list

of Exclusive Businesses that Adi Group and Jamshyd

Group can undertake is as follows:

Both the family groups

have agreed to a non-compete protection for

their Existing Businesses and Exclusive Business,

which would be applicable for a total of 6 years

from the effective date of the FSA (‘Non-Compete

Period’). Post the Non-Compete

Period, each family group would be allowed to

enter into the Exclusive Businesses of the other

group without using the ‘Godrej’

or the names of the corporate entities. The

non-compete obligations in the BNC are subject

to customary exceptions and other pre-agreed

limitations. The trademark ‘Godrej’

will be equally owned and shared by both Adi

Group and the Jamshyd Group. Each of the family

groups shall have the exclusive right to adopt,

use, own and register ‘Godrej’ brand

directly or indirectly for the Existing Businesses

and Exclusive Businesses. The Adi Group shall

have the exclusive right to adopt, use, own

and register the name ‘Godrej’ and

brand for development, marketing of real estate

projects and real estate services relating to

sale and/or purchase, of real estate projects,

and the business of licensing and leasing to

third parties. Jamshyd Group shall

have the exclusive right to adopt, use, own

and register the name ‘Godrej’ and

brand for real estate development business and

the leasing / licensing business carried out

in respect of any land parcels (including the

land in Vikhroli) owned by, or leased as of

January 1, 2024 on a long term basis, to the

Jamshyd Group, directly or indirectly through

their affiliates (‘Existing Land

Holdings’) and also includes

any real estate asset class developed over the

Existing Land Holdings by Jamshyd Group, directly

or indirectly through their affiliates. Adi Group shall not

be restricted, directly or indirectly, from

using ‘Godrej’ brand when acting

as development manager of any land parcel owned

by the Jamshyd Group in Vikhroli (pursuant to

an agreement between Adi Group and Jamshyd Group

and / or their Affiliates). Both family groups

have the non-exclusive right to adopt, use,

own and register ‘Godrej’ name and

brand for ancillary real estate activities such

as project management and consultancy services

for construction projects, construction of hotels,

hospitals and schools, master planning and architectural

designs, etc. For the Shared Businesses,

both family groups can undertake these using ‘Godrej’

brand along with distinguishable group level

differentiators. Shared Business would include

any business not falling under Existing Business

and Exclusive Business and having been agreed

as a shared space for doing business. Few examples

of Shares Businesses include education, hospital,

etc. The Jamshyd Group would

use ‘Godrej Enterprises Group’ or

such other tagline including variations for

its business and the Adi Group would use ‘Godrej

Industries Limited’ or such other tagline

including variations for its business. None

of the family groups can make any modifications

to the stylized Godrej logos (other than to

the color scheme and size of the logo).

Conclusion

Given the unique family dynamics and demographics

in India, such settlements are not uncommon. The

country has witnessed several high-profile family

settlements, such as those of the Ambani and Haldiram

families, which have set precedents for managing

intricate family businesses and wealth divisions.

The Godrej family settlement serves as a valuable

case study for deal makers, highlighting the complexities

and nuances involved in negotiating family agreements.

Authors

Anurag Shah,

Parina Muchhala

and

Nishchal Joshipura

You can direct your queries or comments to the relevant member.

Disclaimer

The contents of this hotline should

not be construed as legal opinion. View detailed disclaimer.

This hotline does not constitute a legal

opinion and may contain information generated using

various artificial intelligence (AI) tools or assistants,

including but not limited to our in-house tool,

NaiDA. We strive to ensure the highest quality and

accuracy of our content and services. Nishith Desai

Associates is committed to the responsible use of AI

tools, maintaining client confidentiality, and adhering

to strict data protection policies to safeguard your

information.

This hotline provides general information

existing at the time of preparation. The Hotline is

intended as a news update and Nishith Desai Associates

neither assumes nor accepts any responsibility for any

loss arising to any person acting or refraining from

acting as a result of any material contained in this

Hotline. It is recommended that professional advice

be taken based on the specific facts and circumstances.

This hotline does not substitute the need to refer to

the original pronouncements.

This is not a spam email. You have received

this email because you have either requested for it or

someone must have suggested your name. Since India has

no anti-spamming law, we refer to the US directive,

which states that a email cannot be considered spam if

it contains the sender's contact information, which

this email does. In case this email doesn't concern you,

please

unsubscribe from mailing list.

|

|

We aspire

to build the next generation

of socially-conscious lawyers

who strive to make the world

a better place.

At NDA, there

is always room for the right

people! A platform for self-driven

intrapreneurs solving complex

problems through research, academics,

thought leadership and innovation,

we are a community of non-hierarchical,

non-siloed professionals doing

extraordinary work for the world’s

best clients.

We welcome

the industry’s best talent -

inspired, competent, proactive

and research minded- with credentials

in Corporate Law (in particular

M&A/PE Fund Formation),

International Tax , TMT and

cross-border dispute resolution.

Write to

happiness@nishithdesai.com

To learn more

about us

Click here.

|

|

Chambers

and Partners Asia

Pacific 2024:

Top Tier for Tax,

TMT, Employment,

Life Sciences, Dispute

Resolution, FinTech

Legal

Legal 500

Asia Pacific 2024:

Top Tier for Tax,

TMT, Labour &

Employment, Life

Sciences & Healthcare,

Dispute Resolution

Benchmark

Litigation Asia

Pacific 2023:

Top Tier for Tax,

Labour & Employment,

International Arbitration

AsiaLaw

Asia-Pacific 2023:

Top Tier for Tax,

TMT, Investment

Funds, Private Equity,

Labour and Employment,

Dispute Resolution,

Regulatory, Pharma

IFLR1000

2024: Top

Tier for M&A

and Private Equity

FT Innovative

Lawyers Asia Pacific

2019 Awards:

NDA ranked 2nd in

the Most Innovative

Law Firm category

(Asia-Pacific Headquartered)

RSG-Financial

Times:

India’s Most

Innovative Law Firm

2019, 2017, 2016,

2015, 2014

|

|

|

|