India Budget Analysis 2025-26

For International Business Community

February 01, 2025

Budget 2025: building foundation for a self-reliant India

As global economic dynamics evolve from globalization

and multilateral cooperation, towards unilateralism;

the growth of Indian economy display signs of resilience

in the midst of changing international status-quo.

India has been actively reshaping its fiscal

framework around the philosophy of self-reliance,

the cornerstone of this government's 'Atma-Nirbhar

Bharat' vision. This recalibration comes amidst

global slowdowns and rising geopolitical tensions,

positioning India as a beacon of resilience and

proactive economic stewardship.

The Union Budget 2025 (“Budget”),

the third under the current NDA government and the

eighth presented by the Finance Minister, reflects

a clear, strategic vision of a 'Vikasit Bharat'

(being a developed India), underpinned by fiscal

prudence and growth-oriented policies. With the

fiscal deficit managed at 4.8% for the current financial

year and a target to reduce it to 4.4% next year,

the Budget emphasizes fiscal consolidation while

carefully balancing the need to fuel economic growth.

This Budget outlines an inclusive growth agenda

(premised on the following key domains of growth –

power, urban development, mining, financial sector,

along with taxation and regulatory reforms), driven

by four pivotal engines of agricultural resilience,

MSME empowerment, reviving investment momentum,

and global export competitiveness. As part of these

initiatives, the Government plans to set up a substantial

Fund of funds exceeding INR 100 billion (~USD 1.15

billion) to boost start-ups, with a particular focus

on deep tech innovations, put strategic emphasis

on artificial intelligence as a key growth driver

for both jobs in industries and overhaul its Bilateral

Investment Treaty models to make India more attractive

destination for global investors. The Budget positions

India as a future-ready export powerhouse, emphasizing

sustainable and high-quality manufacturing. Investments

in green technologies—like electric vehicles,

wind energy, and solar infrastructure—align

with global climate commitments while opening new

economic frontiers. This will aim to provide domestic

value addition and build our clean tech manufacturing

ecosystem (for example, grid scale batteries, PV

cells, motors and controller, etc).

With the aim of encouraging this growth, SWAMIH

Fund 2 will be established as a blended finance

facility with contribution from the Government,

banks and private investors. This year’s Budget

for GIFT City builds on previous reforms, continuing

the Government’s commitment to developing

a robust financial services hub capable of competing

on the global stage. Specifically, the amendments

centre around rationalisation of incentives across

financial products and services, promoting retail

participation and extension of sunset provisions

to ensure continued growth and global competitiveness

of the International Financial Services Centre (“IFSC”).

The Budget puts forth self-reliance as a structural

shift. The Budget proposes a more streamlined, trust-based

regulatory framework, with significant tax reforms

aimed at simplifying compliance. The upcoming Income

Tax Bill promises clearer language and fewer provisions,

with the aim of making tax laws more accessible.

Additionally, a high-level committee has been suggested

for an assessment of all regulatory frameworks for

the non-financial sector with the mandate of making

recommendations for simplification and change on

an annual basis, with the hope that India’s

business environment remains dynamic and responsive.

The Budget has also attempted at understanding pain

points of businesses, with specific initiatives

such as rationalizing the process for business reorganizations –

by widening the fast-track merger process, and attempting

to make the process simpler.

Ease of doing business receives a considerable

boost through initiatives like decriminalizing over

100 statutory provisions, rationalizing customs

tariffs, and modernizing the Central KYC registry.

The introduction of Bharat Trade Net aims to streamline

international trade processes, further enhancing

India’s competitiveness on the global stage.

For the middle class, often the unsung hero of

India's economic resilience, the Budget brings meaningful

relief. A major revamp of personal income tax slabs

effectively eliminates taxes for individuals earning

up to INR1.2 million annually (~USD 13.8k). This

move is expected to boost disposable incomes, spur

domestic consumption, and invigorate sectors reliant

on middle-class spending. The government’s

shift towards a "Trust First, Scrutinize Later"

taxation philosophy reflects a more mature, citizen-centric

approach, promoting voluntary compliance and reducing

the adversarial nature of tax administration. Rationalization

of the TDS provisions is another step towards the

commitment towards simplification.

Small and medium enterprises, which account for

45% of India’s exports, receive targeted support.

The decision to allow 100% Foreign Direct Investment

in the insurance sector (with conditions ensuring

domestic reinvestment) is a bold step towards unlocking

further investment in insurance sector, enhance

competition and improve accessibility to insurance

across the country.

In sum, the Budget reflects the government’s

awareness of both domestic imperatives and global

realities. Through a blend of fiscal discipline,

regulatory reforms, and strategic investments, this

Budget aims to fortify India’s economic foundations

while charting a path towards a more self-reliant,

robust, and inclusive future.

Contents:

1. TAX

RATES

1.1. Companies

-

No Change

in Tax Rates for Domestic Companies; No Extension

for Section 115BAB: Domestic companies

opting for the concessional tax regimes under Section

115BAA and Section 115BAB, will continue to be taxed

at 22% and 15%, respectively, with a surcharge of

10% in both cases. Despite the expectations of the

manufacturing industry, the deadline for new companies

to commence manufacturing or production under Section

115BAB still remains March 31, 2024. Consequently,

the concessional regime will not apply to new companies

starting manufacturing after March 31, 2024.

Domestic companies not availing the concessional

tax regimes will continue be taxed at 30% or 25%,

depending on their turnover for the previous year.

Specifically, a 25% tax rate applies if the turnover

is up to INR 4 billion, and a 30% tax rate applies

otherwise. The surcharge rates for these companies

remain at 7% for total income exceeding INR 10 million

but up to INR 100 million, and 12% for total income

exceeding INR 100 million.

Unchanged

Tax Rates for Foreign Companies: In order

to achieve greater parity, the tax rate for foreign

companies was reduced from 40% to 35% for Financial

Year (“FY”) 2024-25.

The tax rate remains 35% for the FY 2025-26. The

surcharge rates remain unchanged: 2% on total income

exceeding INR 10 million but up to INR 100 million,

and 5% on total income exceeding INR 100 million.

1.2. Individuals

Under Section 87A, an individual resident in

India with an income below INR 0.5 million is eligible

for a 100% tax rebate. This threshold was raised

to INR 0.7 million through the Finance Act, 2023.

For FY 2025-26 onwards, the Bill proposes to further

increase the income limit for which no tax is payable,

from INR 0.7 million to INR 1.2 million, while also

raising the rebate limit from INR 25,000 to INR

60,000. These changes are designed to create a more

equitable tax system and ease the financial burden

on middle-income groups.

|

Old Regime

|

New Regime

(FY 2024-25)

|

New Regime

(FY 2025-26)

|

|

Taxable income

|

Tax rate

|

Taxable income

|

Tax rate

|

Taxable income

|

Tax rate

|

|

Up to INR 2.5 lacs

|

Nil

|

Up to INR 3 lacs

|

Nil

|

Up to INR 4 lacs

|

Nil

|

|

INR 2.5 lacs to 5 lacs

|

5%

|

INR 3 lacs to 6 lacs

|

5%

|

INR 4 lacs to 8 lacs

|

5%

|

|

INR 5 lacs to 10 lacs

|

20%

|

INR 6 lacs to 9 lacs

|

10%

|

INR 8 lacs to 12 lacs

|

10%

|

|

Above INR 10 lacs

|

30%

|

INR 9 lacs to 12 lacs

|

15%

|

INR 12 lacs to 16 lacs

|

15%

|

| |

|

INR 12 lacs to 15 lacs

|

20%

|

INR 16 lacs to 20 lacs

|

20%

|

| |

|

Above INR 15 lacs

|

30%

|

INR 20 lacs to 24 lacs

|

25%

|

| |

|

|

|

Above 24 lacs

|

30%

|

1.3. Co-operative

Societies, Firms, and Local Authorities

For the FY 2025-26, the tax rates and surcharges

for co-operative societies, firms, and local authorities

remain same as those specified for FY 2024-25.

2. Harmonization

of “Significant Economic Presence” with

business connection

Section 9 of the Income-tax Act, 1961 (“ITA”)

is a deeming provision that outlines specific circumstances

under which a non-resident’s income is

deemed to accrue or arise in India, thereby

making it taxable in India. Section 9 contains the

concept of ‘business connection’ which

stipulates that income earned by a non-resident

through or from a business connection in India will

be deemed to accrue or arise in India, and will

therefore be taxable in India.

Section 9 further elaborates what constitutes

business connection and what is carved out from

its meaning. One of the carve outs states that a

non-resident shall not constitute business connection

in India if the operations of the non-resident are

limited to the purchase of goods in India for the

purpose of exporting (“Export Carve-out”).1

Thus, non-residents simply purchasing goods in India

for the purpose of export are not considered as

having ’business connection’ in India.

Introduction of significant economic presence

(“SEP”)

The genesis of SEP can be traced back to the

Organization for Economic Co-operation and Development

(“OECD”) Action Plan

1 (Addressing the tax challenges of digital economy)

under its Base Erosion and Profit Shifting (“BEPS”)

project. The Action Plan 1 discussed several options

to tackle the direct tax challenges arising in digital

business, including introduction of a new nexus

rule based on SEP.2 In furtherance of

the same, through Finance Act, 2018, the concept

of ‘business connection’ was expanded

by introducing the concept of SEP.While introducing

the SEP provisions, the Memorandum to Finance Bill,

2018 noted as follows:

“The

scope of existing provisions of clause (i) of sub-section

(1) of section 9 is restrictive as it essentially

provides for physical presence based nexus rule

for taxation of business income of the non-resident

in India. Explanation 2 to the said

section which defines ‘business connection’

is also narrow in its scope since it limits the

taxability of certain activities or transactions

of non-resident to those carried out through a dependent

agent.

Therefore, emerging business models such as digitized

businesses, which do not require physical presence

of itself or any agent in India, is not covered

within the scope of clause (i) of sub-section (1)

of section 9 of the Act..

In view of the above, it is proposed to amend

clause (i) of sub-section (1) of section 9 of the

Act to provide that significant economic presence'

in India shall also constitute 'business connection'.”

(Emphasis supplied)

The concept of SEP, inter-alia, includes

within its ambit transaction in respect of any goods,

services, or property carried out by a non-resident

with any person in India, including the download

of data or software in India, if the total payments

from such transactions during the previous year

exceed a prescribed amount. In case where a non-resident

has SEP in India, such SEP shall constitute ‘business

connection’ in India.

Interplay of SEP and the Export Carve-Out

Given that the scope of SEP is broad, it could

inadvertently negate the Export Carve-out, creating

a contradiction. To harmonize the provisions and

maintain consistency, The Finance Bill, 2025 (“Bill”)

has proposed an amendment to the definition of SEP.

The amendment clarifies that the transactions or

activities of a non-resident in India, which are

confined to the purchase of goods in India for export,

will not be considered as creating an SEP in India.

This will align the provision with the existing

Export Carve-out, ensuring that such transactions

remain outside the scope of Indian taxation. While

this is a welcome move, it is important to note

that SEP provisions are subject to provisions under

relevant tax treaties (which are generally narrower

in scope than the ITA). Therefore, non-residents

transacting in India through treaty jurisdictions

can claim relief under the tax treaty. The proposed

amendment is to be effective from April 1, 2026,

leaving room for ambiguity for prior periods.

Other issues

While the amendment is welcome, SEP provisions

continue to be broad and vague. This poses further

problems even from a compliance perspective considering

non-residents are mandatorily required to disclose

in their income-tax return whether they have SEP

in India or not. This could have also been

an opportunity for the Government to rationalize

the SEP provisions to align it with the intent of

its introduction.

3.

SOVEREIGN WEALTH FUNDS (“SWFS”)

In order to attract long-term stable capital

from sovereign wealth funds (“SWFs”)

and pension funds (“PFs”),

Finance Act, 2020 exempted certain income in nature

of dividend, interest, long-term capital gains (“LTCG”)

arising from specified investments from tax. The

exemption is provided in case where such investments

were made before on or before March 31, 2025.

In a welcome move, the Bill has proposed to extend

this sunset by 5 years until March 31, 2030. A one-time

extension for 5 years should provide certainty and

clarity to SWFs and PFs for their Indian investments

and help boost the infrastructure sector in India.

In 2024, India’s entrepreneurial growth and

strong policies on the green transition have attracted

SWF investments, enabling 72 of the 473 deals (15%),

valued at USD 17.4 billion.3 The proposed

amendment should attract further capital from SWFs

and PFs in India.

Last year, the Finance (No.2) Act, 2024 re-classified

all capital gains arising from transfer of unlisted

debt securities as short-term capital gains, irrespective

of the holding period. This resulted in an anomaly

considering the exemption under section 10(23FE)

to recognized SWFs and PFs was limited to LTCG and

is available if the investments are held atleast

for 3 years. The Bill now proposes to correct this

anomaly. Pursuant to the amendment, LTCG on transfer

of unlisted bonds or debentures will be exempt in

hands of recognized SWFs and PFs. Gains on transfer

of unlisted bonds or debentures will qualify as

LTCG if such securities are transferred after 2

years from their date of acquisition.

4. ALTERNATIVE INVESTMENT FUNDS

(AIF) TAXATION

section 115UB of the Income Tax Act, 1961

(“ITA”) has accorded

pass-through status to Category-I / Category-II

alternative investment funds regulated under the

SEBI (Alternative Investment Fund) Regulations,

2012 or under the IFSCA (Fund Management) Regulations,

2022 (“Investment Fund”).

As per section 115UB, any income (other than income

in nature of profits and gains from business or

profession) is exempt from tax in hands of an Investment

Fund and taxable directly in hands of its investor.

Further, section 115UB provides that any income

accruing or arising to, or received by, a unit-holder

of an Investment Fund out of investments made in

the Investment Fund shall be chargeable to income-tax

in the same manner as if it were the income accruing

or arising to, or received by such person, had the

investments made by the Investment Fund been made

directly by the unit-holder. Accordingly, the income

of a unit holder in the Investment Fund will take

the character of the income that accrues or arises

to, or is received by the Investment Fund.

Historically, the issue of characterization of

income from transfer of securities (whether taxable

as business income or capital gains) has been a

subject matter of litigation. There have been judicial

pronouncements on whether gains from transfer of

securities should be taxed as ‘business income’

or as ‘capital gains’. In order to reduce

litigation and maintain consistency in approach

in assessments, the Central Board of Direct Taxes

(“CBDT”) issued a circular

instructing that income arising from transfer of

listed shares and securities, which are held for

more than twelve months should be taxed under the

head ‘Capital Gains’ unless the tax-payer

itself treats these as its stock-in-trade and transfer

thereof as its business income.4 However,

this circular covered only listed shares and securities.

Later, the CBDT issued another clarification

stating that income arising from transfer of unlisted

shares should be considered under the head ‘Capital

Gains’ irrespective of the period of holding

(“General Rule”) with

a view to avoid dispute/ litigation and to maintain

uniform approach.5 However, certain exceptions

were provided to the General Rule by CBDT. One such

exception was where transfer of unlisted shares

is made along with control and management of underlying

business. However, considering that Investment Funds

may exercise some form of control and management

in underlying business, based on industry representations,

the CBDT clarified that the aforesaid exception

would not be applicable to Investment Funds. Accordingly,

gains earned by the Investment Funds on transfer

of unlisted shares, even where the transfer is made

along with the control and management of the underlying

business would be characterized as capital gains.

The Bill now proposes to specifically include

any security held by an Investment Fund within the

ambit of ‘capital asset’. Accordingly,

any gains arising from transfer of any security

by an Investment Fund will be in nature of ‘capital

gains’. While a holistic reading of the aforementioned

circular and General Rule leaves little room for

doubt that income arising from transfer of unlisted

shares by an Investment Fund should be regarded

as capital gain income, nonetheless this is a welcome

change. Further while the circular covered only

unlisted shares, now income arising from listed

as well as unlisted shares and any other security

held by an Investment Fund would be regarded as

capital gain income. Category - III Alternate Investment

Funds would nonetheless have to deal with the issue

of characterization of income since these funds

are not covered within the above proposed change.

5. CLARIFICATIONS

FOR FOREIGN PORTFOLIO INVESTORS

Finance (No, 2) Act, 2024 made substantial changes

to the capital gains tax regime in India. The tax

rate on LTCG arising from transfers made on or after

July 23, 2024 was changed to 12.5% (plus applicable

surcharge and cess), irrespective of whether the

transferor is a resident or non-resident.

The tax rates for FPIs are provided in section

115AD (not section 112). While Finance (No, 2) Act,

2024 amended section 115AD to provide that LTCG

arising on transfer of listed equity shares will

be taxable at 12.5% (plus applicable surcharge and

cess), LTCG arising on all other assets continued

to be taxed at rate of 10%. This anomaly is proposed

to be corrected by the Bill. Going forward, any

LTCG arising to an FPI will be subject to tax at

rate of 12.5% (plus applicable surcharge and cess)

6. VDA

TAXATION AND ENHANCED REPORTING

Tax regime for virtual digital assets (“VDAs”)

was introduced by the Finance Act, 2022 under the

ITA. The VDA tax regime was not seen favourably

by the industry resulting in a massive 92% decline

in trading volumes of crypto assets in domestic

markets and migration of users to offshore platforms.6

Reports also estimated that the government potentially

lost INR 24.89 billion (~ USD 287 million) in tax

revenue since February 2022 to January last year

due to reduced volumes on Indian exchanges.7

The crypto industry had requested for several changes

in the VDA tax regime inter-alia including reduction

of withholding tax rate on VDA, allowance for set-off

and carry forward of VDA losses etc. However, these

requests have gone unheard by the government. The

amendments proposed under the Bill are likely to

tighten oversight over crypto-assets.

Information

sharing and due diligence requirements

In 2023, anti-money laundering provisions were

extended to various service providers in the virtual

digital asset ecosystem. The anti-money laundering

provisions were amended to add several compliance

obligations like verification of identity, enhanced

due diligence, maintenance of records by reporting

entities.8 While Finance Act, 2022 had

introduced the tax regime for VDAs, there were no

reporting requirements prescribed for VDA under

the ITA. The Bill proposes to introduce obligation

on ‘reporting entities’ to furnish information

on transactions of crypto-asset (not VDAs). The

persons covered within reporting entities, nature

and manner of maintenance of information by such

reporting entities will be prescribed by the Government

by way of rules. This proposed amendment seems to

be geared towards intermediaries like crypto-exchanges

which are likely to be included within the ambit

of ‘reporting entities’. Rules will

also be prescribed for the due diligence to be carried

out by the reporting entities for purpose of identification

of any crypto-user or owner. This is likely

to increase compliance burden on such ‘reporting

entities’ and they will have to put in place

arrangements to ensure that data is collected properly

for reporting to government. Further, what liability

/ penalties may apply in case of non-compliance

is not clear currently.

For the purposes of the aforesaid information

reporting, the Bill proposes to add another limb

to the definition of VDA. The proposed definition

includes within its ambit any crypto-asset being

a digital representation of value that relies on

a cryptographically secured distributed ledger or

a similar technology to validate and secure transactions,

whether or not such asset is included in the earlier

limbs of VDA or not. Unlike the earlier limbs of

VDA definition, this new limb includes crypto-assets

that rely on blockchain technology (or similar technology)

to validate and secure transactions only. Therefore,

reporting obligations would be limited to such crypto-assets.

This change seems to be in line with the global

movement on crypto-asset reporting framework proposed

by OECD which allows for automatic exchange of tax

relevant information on crypto-assets.

Search

provisions amended to include VDA within ambit of ‘undisclosed

income’

The Bill has proposed to add VDA within the ambit

of ‘undisclosed income’ under Chapter

XIV-B (Special procedure for assessment of search

cases) of the ITA. The provisions empower tax authorities

to conduct block assessments in cases where search

is conducted. Income determined under such block

assessment is taxed at rate of 60%. The time-limit

for completion of block assessment is proposed to

be made as twelve months from end of the quarter

in which the last of the authorisations for search

or requisition has been executed. This amended is

likely to significantly impact crypto traders specifically

in cases where income from crypto transactions has

been undisclosed. A positive impact (and intended

impact) of this change may be to bring the crypto-transactions

on regulated platforms such that the transactions

do not go undetected.

On an overall basis, while to substantive changes

have been made to VDA tax regime, the proposed changes

clearly indicate government’s intent to keep

a close eye and monitor crypto transactions in the

country.

7. GIFT

CITY INCENTIVES

7.1 Extension

of Sunset Clauses

The Government has introduced several tax concessions

to encourage the establishment and growth of businesses

set up in the IFSC at GIFT City. These concessions

are currently available under various provisions

of the ITA and are aimed at making the IFSC a global

financial hub. However, these benefits are subject

to sunset dates, after which they would no longer

apply. Currently, the deadline for many of these

concessions is March 31, 2025.

To further promote the development of the IFSC

and attract international financial activities,

the Bill proposes to extend the sunset dates for

these concessions to March 31, 2030. The revised

sunset dates apply to the following sections of

the ITA:

|

Section

|

Exemption

|

|

80LA (2)(d)

|

Income arising from transfer of an aircraft

or a ship leased by a unit in IFSC to a

person, provided that the unit should have

commenced operations on or before March

31, 2030.

|

|

10(4D)

|

Income from a securitisation trust (which

is chargeable under the head "Profits and

Gains of Business or Profession") to the

extent such income is attributable to the

investment division of offshore banking

unit which has commenced its operations

in the IFSC on or before March 31, 2030.

|

|

10(4F)

|

Royalty or Interest income in the hands

of non-residents from leasing aircrafts

or ships to a unit which has commenced operations

in the IFSC on or before March 31, 2030.

|

|

10(4H)

|

Capital gains income in the hands of

non-residents engaged in aircraft leasing

or aircraft leasing units in the IFSC,

from the transfer of equity shares of an

aircraft leasing unit which has commenced

operations in the IFSC on or before March

31, 2030.

|

|

47(viiac)

47(viiad)

|

Capital gains income the relocation of

an offshore to the IFSC, where the relocation

takes place on or before March 31, 2030.

|

|

9A(8A)

|

Government’s power under Section

9A(8A) to modify eligibility conditions

in relation to offshore funds managed by

IFSC-based managers which have commenced

operations on or before March 31, 2030.

|

While the extensions are a step in the right

direction, the do not fully resolve the uncertainty

regarding the long-term availability of these exemptions.

The limited duration of the concessions may hinder

long-term tax planning and affect stakeholder’s

willingness to make substantial investments in GIFT

City.

7.2 No

more premium caps for IFSC life insurance policies

Under Section 10(10D) of the ITA, the sum received

under a life insurance policy, including any bonuses,

is exempt from tax, subject to certain conditions.

However, the exemption does not apply to unit-linked

insurance policies (“ULIPs”)

where the annual premium exceeds INR 0.25 million,

nor to life insurance policies where the annual

premium exceeds INR 0.5 million, excluding ULIPs.

These provisions currently apply to policies issued

by Insurance Offices in the IFSC.

This creates a disadvantage for non-residents

purchasing life insurance from IFSC Insurance Offices

compared to policies from foreign jurisdictions,

where no such premium caps exist. To address this

disparity and encourage non-residents to avail life

insurance services from IFSC Insurance Offices,

the Bill proposes to remove the premium cap restrictions

for policies issued by IFSC Insurance Offices. This

change is also in line with the Government’s

general push to further expand the retail insurance

market in the IFSC.

7.3 Exemption

on income from Specified Derivatives entered into

with FPIs in GIFT City

Section 10(4E) of the ITA provides for an exemption

on any income accrued, arisen or received by a non-resident

as a result of (i) the transfer of; or (ii) distributions

from, non-deliverable forward contracts, offshore

derivative instruments, or over-the-counter derivatives

(“Specified Derivatives”)

entered into with a banking units set up in the

IFSC.

The Bill proposes to amend clause 10(4E) to extend

the same tax exemption to income earned by a non-resident

in relation to Specified Derivatives entered into

with Foreign Portfolio Investors (“FPIs”)

set up in the IFSC.

This amendment follows a SEBI circular issued

on June 27, 2024 whereby the cap permitted for participation

by NRI/ OCI/RIs in a single FPI was increased from

less than 50% to up to 100% of the FPI’s corpus.

These changes are clearly intended to further

promote the set-up of FPIs in IFSC as opposed to

other jurisdictions like Mauritius and Singapore,

which is in line with the Government’s objective

of providing a tax and regulatory framework in GIFT

City which is on par with or better than other global

jurisdictions.

The change is expected to take effect from April

1, 2026.

7.4. Capital

gains and dividend exemptions for ship leasing in

the IFSC:

The Bill proposes to provide an exemption for

capital gains income in the hands of (i) non-residents

and (ii) IFSC units, engaged in ship leasing from

the transfer of equity shares of a ship leasing

company in the IFSC. The Bill further proposes to

provide an exemption on dividends paid by one ship

leasing company in the IFSC to another.

These changes are intended to align the tax treatment

of ship leasing with that of aircraft leasing, given

the similarities in their business structures and

investor protection mechanisms, such as the use

of special purpose vehicles (“SPVs”)

for individual vessels.

Rationalisation

of definition of ‘dividend’ for treasury

centres in the IFSC

Under Section 2(22)(e) of the ITA, the definition

of "dividend" includes certain advances or loans

made by a company to its shareholders or affiliated

concerns. Specifically, amounts paid to a shareholder

holding at least 10% of the voting power in a private

company or substantial interest in a concern are

deemed to fall within the meaning of dividend.

The Bill has proposed to exclude payments in

the nature of loans or advances between two group

entities from the definition of dividend under the

ITA, provided that (i) one of the group entities

is a Finance Company or Finance Unit registered

with the IFSCA for undertaking activities or services

as a global or regional corporate treasury centre,

and (ii) the parent entity or principal entity of

such group is listed on an offshore stock exchange.

This amendment is designed to promote economic

growth, improve global business operations, and

attract foreign investment into the IFSC, aligning

with the broader objective of enhancing India’s

financial services ecosystem.

7.5. Expansion

of Tax-Neutral Relocations to Retail Schemes and

Exchange Traded Funds (“ETFs”) in IFSC

Certain provision of the ITA provides a tax neutral

relocation of an offshore fund to the IFSC provided

that the resultant fund in the IFSC is granted registration

as a Category I, II or III AIF under the IFSCA (Fund

Management) Regulations, 2022 (“FM

Regulations”). This exemption is

now proposed to be extended to relocations wherein

the resultant fund is registered as a retail scheme

or exchange traded fund registered under the FM

Regulations.

As on May 31, 2024, 12 funds had relocated from

various jurisdictions to GIFT IFSC with a targeted

commitment of approximately USD 5 Billion. The proposed

amendment has been introduced to further catalyse

such relocations and boost retail participation

in the IFSC. However, only time will tell whether

such exemption will actually be enough to incentivize

the relocation of funds already well established

in foreign jurisdiction. The exemption is expected

to take effect from April 1, 2026.

8. NO

EVERGREENING OF LOSSES ON MERGER

Sec 72A of the ITA provides for the carry-forward

and set-off of accumulated losses and unabsorbed

depreciation allowance in case of amalgamation,

demerger, business reorganisation etc. Section 72A(1)

provides that the accumulated loss and unabsorbed

depreciation of the amalgamating company are deemed

to be loss or the unabsorbed depreciation of the

amalgamated company for the previous year in which

the amalgamation was effected. Section 72A(6) provides

a similar provision in the case of business reorganisation

whereby a company succeeds a firm or proprietary

concern. Further, Section 72A(6A) provides a similar

provision in the case of business reorganisation

whereby a Limited Liability Partnership succeeds

a private company or unlimited public company. While

generally, as per business losses cannot be carried

forward for more than 8 FYs from the FY in which

the loss was first computed, in situations like

amalgamations/ business reorganisation, the loss

of predecessor entity gets a fresh life in hands

of the successor entity. This provided the opportunity

for the evergreening of losses of the predecessor

entity by undertaking amalgamation, business reorganization,

or demerger.

The Bill proposes an end this by amending section

72A of the ITA to provide for no carry forward and

set off of accumulated loss after eight FYs from

the immediately succeeding FY for which such loss

was first computed for original predecessor entity.

The amended provision applies to amalgamation or

business reorganisation effected on or after April

1, 2025.

While the proposed amendment is likely to impact

carry forward of losses in cases of conversion of

firm / proprietary concern into company or conversion

of a private company / unlisted public company into

an limited liability partnership in a tax neutral

manner. In cases where such conversions are not

undertaken in tax neutral manner (i.e. without fulfilling

conditions under section 47), carry forward of losses

is not permitted under the ITA.

In so far as carry forward of losses in amalgamations

is concerned, carry forward of losses is allowed

only in certain cases like amalgamation of company

owning an industrial undertaking or ship or hotel

with another company etc. The proposed amendment

is likely to have an impact on such amalgamation

schemes pending approval from Court. Importantly

for mergers, the amended provision will apply from

the effective date i.e. date of approval from court

irrespective of the appointed date9 in

the scheme.

9. PRESUMPTIVE

TAX REGIME FOR NON-RESIDENTS PROVIDING TECHNOLOGY

/ SERVICES TO ELECTRONIC MANUFACTURING

To advance the Aatmanirbhar Bharat vision, and

establish India as a global Electronics System Design

and Manufacturing (“ESDM”) hub (in line

with the National Policy on Electronics), the Indian

Government launched a >USD 10 billion program

for developing the semiconductor and display manufacturing

ecosystem in India, with targeted schemes to attract

investments and provide incentives for manufacturing

in India.10 This initiative aims to strengthen

India's electronics manufacturing ecosystem and

boost foreign and domestic participation.

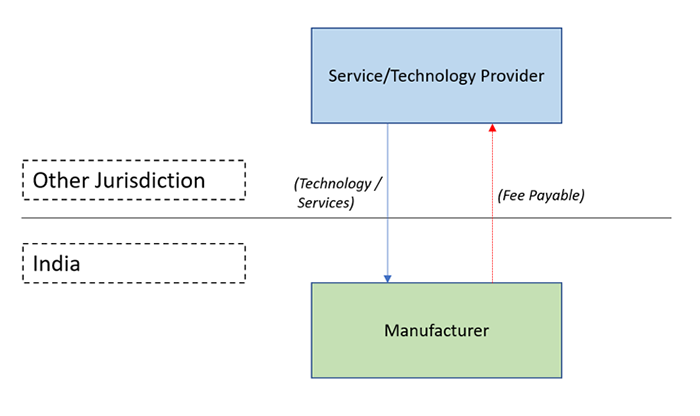

Typically, business models involve a non-India

entity which develops, owns, and licenses the intellectual

properties with respect to the semiconductors –

to group entities, or third-party manufacturers

or distributors across the world (including a manufacturing

entities in India). Such non-India entities (or

other group entities with experience in development

and design of semi-conductors) may also provide

other services to the Indian manufacturers (for

example, product and chip-layout designs; engineering

or technical advisory with respect to the manufacturing

process; or provide any other technical know-how

for the semiconductors).

Subject to a case by case determination of facts

- the license fee payable for the transfer of rights

in respect of relevant patents, inventions, models,

designs, secret processes (or the imparting of information

in their respect); or the imparting of any other

information concerning the technical, industrial,

commercial or scientific knowledge, experience or

skill - may qualify as ‘royalty’ as

per the Income Tax Act (which attracts a withholding

tax in India at the rate of 20%). Similarly, service

fee payable by the Indian manufacturers to such

non-Indian entities for rendering any managerial,

technical, or other consulting services –

may qualify as ‘fee for technical services’

as per the Income Tax Act, based on the specific

facts of the case (which also attracts a withholding

tax in India at the rate of 20%).

In both these scenarios, if the non-resident

is eligible to avail the benefit of a narrower definition

of ‘royalties’ or ‘fee for technical

services’ (or a ‘make available’

clause in the treaty which requires the technical

service be made available to the resident) –

they may be able to escape the Indian withholding

tax net. However, given the business models, if

such fees payable by the Indian manufacturers also

qualify as ‘royalties’ or ‘fee

for technical services’ under the relevant

treaties – they may nonetheless be able to

avail a beneficial lower withholding tax rate of

10% to 15%, depending on the treaty. Further,

provision of technology or services (by non-residents)

may at times also create the risk of a potential

permanent establishment of such non-resident being

constituted in India. While the risk would be based

on the specific facts of each case – income

attributable to such a permanent establishment is

taxable at the applicable rate for non-residents

(i.e., 35% plus applicable surcharge and cess).

The introduction of Section 44BBD by the Bill

is a significant and beneficial step toward bolstering

India's position as a global hub for Electronics

System Design and Manufacturing (ESDM).

Section 44BBD proposed to be introduced by the

Bill, sets out a presumptive taxation regime for

non-resident entities engaged in providing technology

or services in India, for (a) setting up or operating

electronics manufacturing facilities; or (b) in

connection with manufacturing or producing electronic

goods, article or things in India. This is subject

to two mandatory conditions required to be met by

the Indian companies receiving the technology or

services –

The Indian company should be establishing or

operating electronic manufacturing facilities, or

connected facilities (under a scheme notified by

the Central Government and MEITy); and The Indian company should satisfy such other

conditions as may be prescribed.

By way of the presumptive tax regime - 25% of

the aggregate receipts of such non-residents are

deemed to be profits and gains from business of

the non-resident. Given the corporate tax rate of

35% (plus applicable surcharge and cess) for foreign

companies in India, this implies an effective tax

payable of less than 10% on gross receipts. The

taxable receipts shall include amounts paid / payable

to the non-resident (or any person on their behalf)

for the technology or services; and also includes

amounts received (or deemed to be received) by or

on behalf of such non-residents.

The newly introduced provision is expected to

take effect from April 01, 2026, prospectively.

However, for those non-residents who are eligible

to claim treaty benefits (as set out above) –

this provision should not now imply any additional

tax implications in India. Even for those with claiming

reduced withholding rates under relevant treaty

treaties, the presumptive tax regime may nonetheless

serve as a more certain and plausible option (with

the exception of scenarios where the non-resident

is able to claim a complete exemption from the withholding

tax as per the treaty).

The introduction of the provision thus serves

as a beneficial step to bolster India’s commitment

towards positioning itself as a global hub for Electronics

System Design and Manufacturing (ESDM); and is aligned

with the government's broader objective of making

India a global leader in high-tech manufacturing.

The simplified taxation framework not only reduces

administrative burdens but also encourages greater

foreign participation in India's semiconductor and

electronics manufacturing ecosystem.

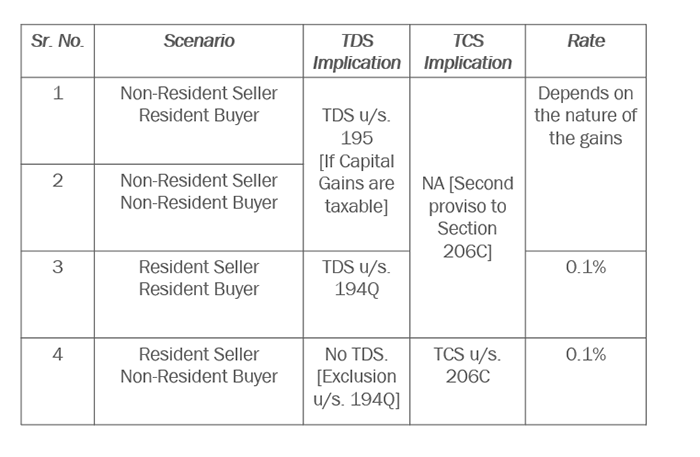

10. TCS Rationalisation

TCS

on Sale of Goods

The provisions of Tax Deduction at Source (“TDS”)

under Section 194Q and Tax Collection at Source

(“TCS”) under Section

206C of the ITA have been key mechanisms to ensure

tax compliance in commercial transactions.

Section 194Q requires buyers to deduct TDS at

0.1% on payments exceeding INR 5 million for the

purchase of goods, while Section 206C(1H) requires

sellers to collect TCS at the same rate on similar

transactions. Section 206C(1H) includes a proviso,

stating that the provision shall not apply to transactions

already subject to TDS. However, given the similarity

in the provisions, sellers faced difficulty in ensuring

that buyers comply with the TDS provisions under

Section 194Q. This has led to the unintended consequence

of both TDS and TCS being applicable on the same

transaction, which complicates the compliance process

and increases the administrative burden on taxpayers.

To address these concerns, it is proposed that

the provisions of Section 206C(1H) will no longer

apply from April 1, 2025.

This change brings much-needed relief by reducing

excessive compliance requirements. Both TDS and

TCS were introduced to ensure taxes are deducted

or collected at the point of transaction, minimizing

the risk of non-payment or underreporting. However,

since both provisions served the same purpose, having

them in parallel only added to the taxpayer's compliance

burden. Additionally, while TDS is deducted by the

buyer with the seller claiming credit, TCS requires

the seller to collect tax from the buyer, even when

the buyer has no taxable income on the purchase

transaction.

Furthermore, the rationalization provides clarity

from a transactional perspective. The ITA does not

define the term 'goods,' as outlined in both Section

206C(1H) and Section 194Q. In this context, reference

was made to the Sale of Goods Act, which includes

items such as shares and securities within the definition

of goods. Consequently, both the provisions were

interpreted to apply to these financial instruments.

As a result, TDS and TCS on such transactions (if

taxable) are currently as follows:

Following the Bill, the rationalization will

eliminate the requirement for TDS or TCS in transactions

involving a Resident Seller and a Non-resident Buyer,

potentially providing relief to taxpayers engaged

in such transactions.

Rationalisation

of TCS on Remittances under RBI's Liberalized Remittance

Scheme (LRS)

In a bid to enhance ease of transactions and

provide relief to taxpayers, the Bill proposes to

include significant changes to the TCS provisions

concerning remittances under the Reserve Bank of

India’s (“RBI”)

Liberalized Remittance Scheme (“LRS”).

Increase

in TCS Threshold

The threshold for collecting tax at source on

remittances under the LRS is set to rise from INR

0.7 million to INR 1 million. This increase is expected

to benefit taxpayers making cross-border transactions,

as it raises the limit before TCS becomes applicable.

Removal

of TCS on Education-related Remittances

In a noteworthy move, the Bill also seeks to

remove TCS on remittances made for educational purposes.

This applies specifically when the remittance is

financed through a loan obtained from a specified

financial institution. The definition of a “specified

financial institution” under Section 80E(3)(b)

includes:

A banking company regulated

by the Banking Regulation Act, 1949 Any other financial

institution that the Central Government may

specify via a notification in the Official Gazette.

These changes are designed to streamline the

process and provide relief to taxpayers, particularly

those remitting funds for educational purposes using

loans from recognized financial institutions.

11. Three-Year Block Approach

for Determining Arms’ Length Price

Transfer pricing provisions under the ITA require

income arising from international transactions or

specified domestic transactions (“SDTs”)

between associated enterprises to be computed having

regard to the arm’s length price (“ALP”)11.

The ITA also provides a detailed methodology for

determining the ALP in such transactions12.

The assessment proceedings of such taxpayers involve

the Assessing Officer (“AO”)

referring the determination of ALP to the Transfer

Pricing Officer (“TPO”)13.

Once the TPO determines the ALP, the AO adjusts

the taxpayer's total income in accordance with the

TPO’s order14.

Typically, entities engage in similar international

transactions or SDTs on a yearly basis. Consequently,

the process of referring these transactions to the

TPO for ALP determination is repeated annually.

Given the complexity and administrative burden of

this process, the Bill proposes to introduce Section

92CA(3B), providing an option to taxpayers to apply

the same ALP to “similar international transactions

or SDTs” for a block of three years. Under

the amendments:

Taxpayers must file

a prescribed form within the specified timeframe

to exercise the option. The TPO will assess

the validity of the option and issue an appropriate

order within one month of its exercise, determining

whether the transactions are similar and valid. Once confirmed, the

ALP determined for an international transaction

or SDT in the given year will be applied by

the AO to similar transactions or SDTs for the

two consecutive years immediately following

that year.

This benefit, however, is not extended to search

cases separately dealt with under Chapter XIV-B.

Further, pertinent to note that the option seems

to be available on a per-transaction and not a per-year

basis.

This amendment marks a positive step in reducing

compliance burdens and redundancy in transfer pricing

proceedings by minimizing the need for multiple

ALP determinations for the same or similar transactions

across years. However, several practical aspects

remain unclear.

Firstly, the time limit for filing the prescribed

form is yet to be specified. While the option is

set to be available starting April 1, 2026, allowing

taxpayers to file the form from that date, its applicability

to financial years with open or pending proceedings

will depend on the time limit eventually prescribed

for the filing. Additionally, the amendment does

not address the validity of this option in case

there are changes in facts or the transactions in

subsequent years.

Moreover, the term "similar international transaction"

is not defined. This could lead to complications,

as transactions that are similar but involve different

parties or circumstances each year may raise questions

about how to categorize them.

In addition to above, to reduce litigation and

provide greater certainty in international taxation,

the Finance Minister in the Budget Speech proposed

to expand the scope of safe harbour rules. As a

result, these rules may be subject to amendments.

- International Tax Team

You can direct your queries or comments to the authors.

1Clause (b) of Explanation 1 to Section

9(1)(i)

2Memorandum to the Finance Act, 2018,

page 8.

3Sovereign Wealth Funds 2024: resilience

and growth in a new global landscape; available

at:

https://static.ie.edu/CGC/SovereignWealthFunds_2024report_IECGC.pdf

4Circular No. 6 of 2016 dated February

29, 2016

5Instruction No. F.No. 225/12/2016/

ITA.II dated May 2, 2016

6‘Web3 growth hinges

on taxation reforms: A Budget Wishlist’ available

at

https://economictimes.indiatimes.com/markets/cryptocurrency/web3-growth-hinges-on-taxation-reforms-a-budget-wishlist/articleshow/117542929.cms?from=mdr

7‘The impact of India's 1% TDS

on Virtual Digital Assets: A call for reform’

available at

https://economictimes.indiatimes.com/markets/cryptocurrency/the-impact-of-indias-1-tds-on-virtual-digital-assets-a-call-for-reform/articleshow/111599629.cms?from=mdr

8Prevention of Money Laundering Act,

2002

9Appointed date is the specific date

designated within a scheme, from which the transactions

of the merger are considered to have occurred

10https://www.meity.gov.in/esdm/Semiconductors-and-Display-Fab-Ecosystem

11Section 92 of the ITA

12Section 92C of the ITA

13Section 92CA(1)

14Section 92CA(4)

Disclaimer

The contents of this hotline should

not be construed as legal opinion. View detailed disclaimer.

This hotline does not constitute a legal

opinion and may contain information generated using

various artificial intelligence (AI) tools or assistants,

including but not limited to our in-house tool,

NaiDA. We strive to ensure the highest quality and

accuracy of our content and services. Nishith Desai

Associates is committed to the responsible use of AI

tools, maintaining client confidentiality, and adhering

to strict data protection policies to safeguard your

information.

This hotline provides general information

existing at the time of preparation. The Hotline is

intended as a news update and Nishith Desai Associates

neither assumes nor accepts any responsibility for any

loss arising to any person acting or refraining from

acting as a result of any material contained in this

Hotline. It is recommended that professional advice

be taken based on the specific facts and circumstances.

This hotline does not substitute the need to refer to

the original pronouncements.

This is not a spam email. You have received

this email because you have either requested for it or

someone must have suggested your name. Since India has

no anti-spamming law, we refer to the US directive,

which states that a email cannot be considered spam if

it contains the sender's contact information, which

this email does. In case this email doesn't concern you,

please

unsubscribe from mailing list.

|

|

We aspire

to build the next generation

of socially-conscious lawyers

who strive to make the world

a better place.

At NDA, there

is always room for the right

people! A platform for self-driven

intrapreneurs solving complex

problems through research, academics,

thought leadership and innovation,

we are a community of non-hierarchical,

non-siloed professionals doing

extraordinary work for the world’s

best clients.

We welcome

the industry’s best talent -

inspired, competent, proactive

and research minded- with credentials

in Corporate Law (in particular

M&A/PE Fund Formation),

International Tax , TMT and

cross-border dispute resolution.

Write to

happiness@nishithdesai.com

To learn more

about us

Click here.

|

|

Chambers

and Partners Asia

Pacific 2024:

Top Tier for Tax,

TMT, Employment,

Life Sciences, Dispute

Resolution, FinTech

Legal

Legal 500

Asia Pacific 2024:

Top Tier for Tax,

TMT, Labour &

Employment, Life

Sciences & Healthcare,

Dispute Resolution

Benchmark

Litigation Asia

Pacific 2024:

Top Tier for Tax,

Labour & Employment,

International Arbitration

AsiaLaw

Asia-Pacific 2024:

Top Tier for Tax,

TMT, Investment

Funds, Private Equity,

Labour and Employment,

Dispute Resolution,

Regulatory, Pharma

IFLR1000

2024: Top

Tier for M&A

and Private Equity

FT Innovative

Lawyers Asia Pacific

2019 Awards:

NDA ranked 2nd in

the Most Innovative

Law Firm category

(Asia-Pacific Headquartered)

RSG-Financial

Times:

India’s Most

Innovative Law Firm

2019, 2017, 2016,

2015, 2014

|

|

|

|